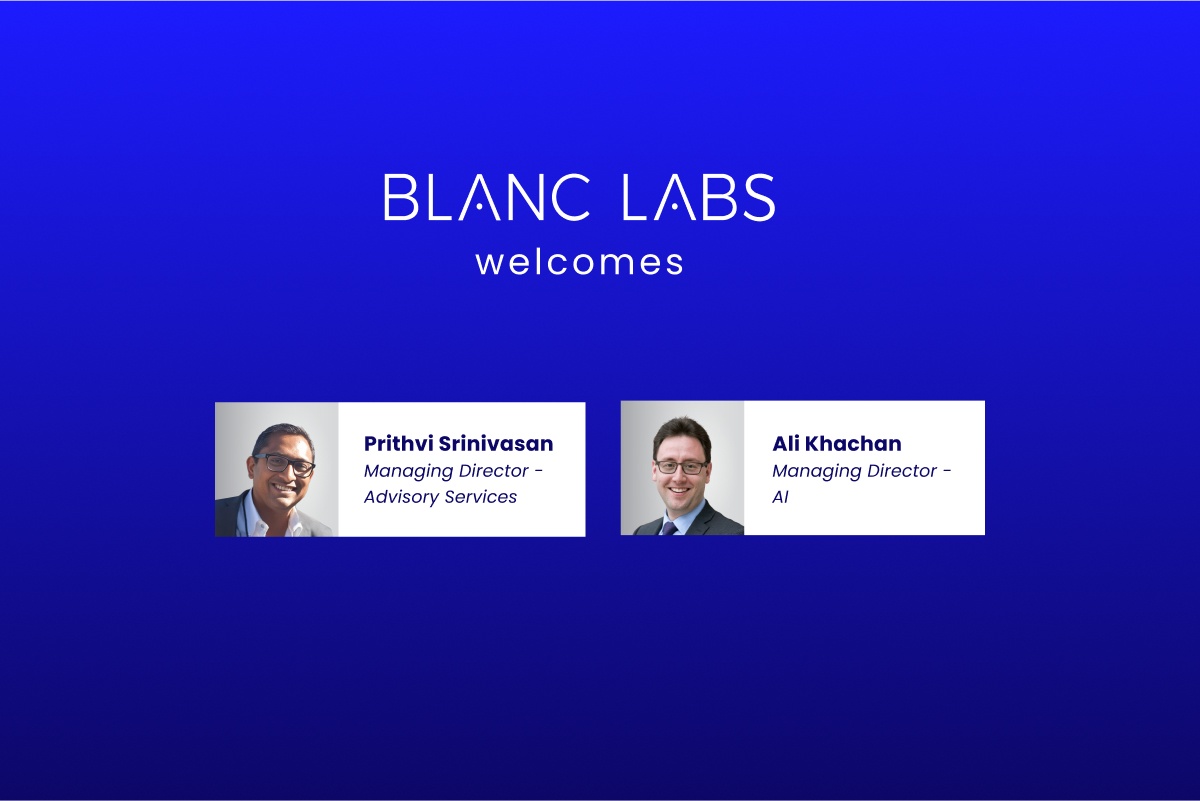

Blanc Labs Welcomes Two New Leaders to Advance AI Innovation and Enhance Tech Advisory Services for Financial Institutions Across North America

May 7, 2024

May 6 (Toronto, ON)— Blanc Labs, a pioneer in Lending Technology, Artificial Intelligence (AI) and Intelligent Automation, is thrilled to announce the appointment of two new members to its executive team, Prithvi Srinivasan and Ali Khachan, both distinguished leaders in technology and consulting.

Prithvi Srinivasan, a former Partner at Deloitte Consulting, is joining Blanc Labs as the Managing Director for Advisory Services. Prithvi brings a wealth of expertise in technology strategy, digital transformation, and business operations excellence, and specializes in driving mission-critical transformation programs. Leveraging his extensive experience in aligning technology initiatives with business value, Prithvi is set to propel financial institutions forward using Blanc Labs’ expertise in lending technology, AI, and intelligent automation. His proven track record in driving successful enterprise transformations and optimizing technology estates underscores his commitment to fostering innovation and delivering value to clients. Prithvi excels in transforming complex strategies into actionable successes, ensuring technology not only meets but advances business objectives.

Ali Khachan, a tech startup leader and former Principal at Boston Consulting Group (BCG), joins Blanc Labs as Managing Director of AI. As a strategic operator with over 15 years of leadership at the nexus of technology and business, Ali has demonstrated a keen ability to drive transformational growth through AI and digital innovations. His expertise in scaling up ventures, spearheading digital transformations, and maximizing value creation for global enterprises will play a pivotal role in shaping the future of Blanc Labs as it continues to pioneer groundbreaking AI solutions.

“The addition of Prithvi and Ali to our executive team significantly strengthens Blanc Labs’ strategic capabilities and reinforces our position as a leading technology partner for the financial sector,” said Hamid Akbari, CEO of Blanc Labs. “Their exceptional expertise and visionary leadership will accelerate our strategic initiatives across Advisory Services, Data, Automation, Artificial Intelligence, and Generative AI solutions. I am confident that with Prithvi and Ali on board, Blanc Labs will achieve new heights in delivering exceptional value to our clients and shaping the future of digital transformation in the financial services industry.”

Both Prithvi and Ali will be speaking at the Canadian Lenders Association Bankers Summit in Toronto on May 15th. They will conduct a series of workshops focused on AI in Lending, demonstrating Blanc Labs’ commitment to fostering knowledge exchange and leading the charge in AI solutions for financial services. To register for the workshops, please reach out to Blanc Labs through their website.

ABOUT BLANC LABS

Blanc Labs is a preferred partner for enterprises looking to digitize and build the next generation of technology products and services. To help companies rapidly deliver on their digital initiatives, Blanc Labs has developed expertise and bespoke solutions in a wide variety of applications in financial services, healthcare, enterprise productivity, and customer experience. Headquartered in Toronto, Blanc Labs serves the Americas through operations in Toronto, New York, Bogota, and Buenos Aires. For more information on how Blanc Labs is building a better future, visit www.blanclabs.com.

Blanc Labs Partners with TCG Process to Integrate their Automation and Orchestration Platform and deliver Advanced Intelligent Workflow Automation to Financial Institutions

Blanc Labs Partners with TCG Process to Integrate their Automation and Orchestration Platform and deliver Advanced Intelligent Workflow Automation to Financial Institutions

May 3, 2024

May 3, 2024 (Toronto, ON) – Blanc Labs, a leader in Lending Technology, AI, and Business Process Improvement, is excited to announce a strategic partnership with TCG Process, leveraging their DocProStar platform to transform lending operations for mid-tier banks, credit unions, and other mortgage origination and servicing providers in Canada. This partnership marks a significant milestone in Blanc Labs’ mission to enhance operational efficiencies and unlock new revenue opportunities for lenders through cutting-edge technology.

Blanc Labs’ Intelligent Automation Methodology, designed by seasoned experts, pinpoints and addresses critical areas for improvement within document intensive workflows. The solution seamlessly integrates with existing technology infrastructure, enabling rapid deployment and immediate impact on operational efficiencies, with minimal investment.

“Rapid advancements in powerful new AI technologies like LLMs are further unlocking opportunities to move away from manual, data heavy workflows that cause frustrations for customers and lending teams alike,” said David Offierski, VP of Partnerships for Blanc Labs. “We are seeing a significant shift from the manual ingestion of customer information to a much more efficient and automated workflow solution, allowing stakeholders to improve both customer and employee experience while reducing operational costs.”

TCG Process’ DocProStar provides intelligent document ingestion, orchestrated processing and powerful AI capabilities that will enable Blanc Labs to quickly deploy advanced, cost-effective, and scalable solutions to meet the unique needs of lending teams.

The collaboration between Blanc Labs and TCG Process signifies a joint commitment to deliver innovative solutions, leveraging cutting-edge technologies to streamline lending processes. The opportunity is clear: to create a more seamless experience for customers, tailored to the unique needs of the Canadian lending market.

“Our partnership with Blanc Labs is more than just technology—it’s about shared expertise and collaboration. By combining our strengths, we will provide industry leading solutions that cater to the diverse needs of the financial services sector.” Joseph Capone, Chief Revenue Officer, TCG Process (Canada).

Hamid Akbari, CEO of Blanc Labs, said, “The use of technologies like DocProStar and our Kapti platform can greatly improve compliance, increase customer retention, reduce servicing cost, and boost revenue in the lending sector. Our deep expertise in lending technologies, and especially intelligent processing of mortgage documents, enhances our role as a transformation partner.”

Blanc Labs operates with agile, expert teams, ensuring that clients typically see a return on their investment within 12 months. The company remains dedicated to its role as a pivotal player in lending industry transformation.

ABOUT BLANC LABS

Blanc Labs is a preferred partner for enterprises looking to digitize and build the next generation of technology products and services. To help companies rapidly deliver on their digital initiatives, Blanc Labs has developed expertise and bespoke solutions in a wide variety of applications in financial services, healthcare, enterprise productivity, and customer experience. Headquartered in Toronto, Blanc Labs serves the Americas through operations in Toronto, New York, Bogota, and Buenos Aires. For more information on how Blanc Labs is building a better future, visit www.blanclabs.com.

ABOUT TCG PROCESS

TCG Process, with headquarters in Switzerland, is an international organization that develops and integrates input management and intelligent process automation software. Its solutions are used in industries such as banking, insurance, healthcare, government, and public administration to digitize and automate document-driven processes. TCG Process sells both directly and via partners globally. Visit www.tcgprocess.com

For media inquiries, please contact:

Shriya Ghate

Senior Marketing Manager

Blanc Labs

E: shriyag@blanclabs.com

Tracy Weller-McCormack

Head of Marketing, Canada & Australia

E: tracy.mccormack@tcgprocess.com

The Transformative Influence of Large Language Models (LLMs) on Document Processing

Financial Services | Banking Automation | Business Process Improvement

Business Process Improvement vs Business Process Reengineering

April 8, 2024

Your business’s ability to change goes a long way toward contributing to long-term success. But how do you decide whether to make small changes over the long term or if a situation calls for a radical change?

To determine this, you must understand business process improvement (BPI) and reengineering (BPR). In this guide, we explain the meaning of BPI and BPR and when to use them.

What is Business Process Improvement?

Business process improvement is an ongoing process where you make small, continuous improvements to make processes more efficient.

BPI is like fine-tuning your car’s engine to make it run smoother and faster. You start by examining the engine’s current condition. Then you find areas that could use some maintenance and perform that maintenance to improve efficiency. Of course, BPI requires careful planning and execution, so it’s always smart to have a BPI specialist by your side.

Continuous improvement and data-driven decisions are key aspects of BPI. Instead of blindly chasing market trends and investing in expensive tech, you start with introspection. You use analytics to validate the need for change. And you make small changes over time to minimize disruption.

What is Business Process Reengineering?

Business process reengineering is a comprehensive process redesign exercise that helps a business improve efficiency and overall performance significantly.

Business Process Reengineering is the radical redesign of business processes to achieve dramatic improvements in productivity, cycle times, quality, and employee and customer satisfaction.

There are times when your business might need a radical change, such as:

When you want to build a competitive advantage

To prepare for rapid growth

After a merger or acquisition

Organizations restructuring

Of course, this is an inclusive list. You might choose to reengineer a process to improve productivity, comply with new regulatory requirements, or introduce new technology. However, BPR is a far more extensive process than BPI. It requires effective change management and stakeholder engagement.

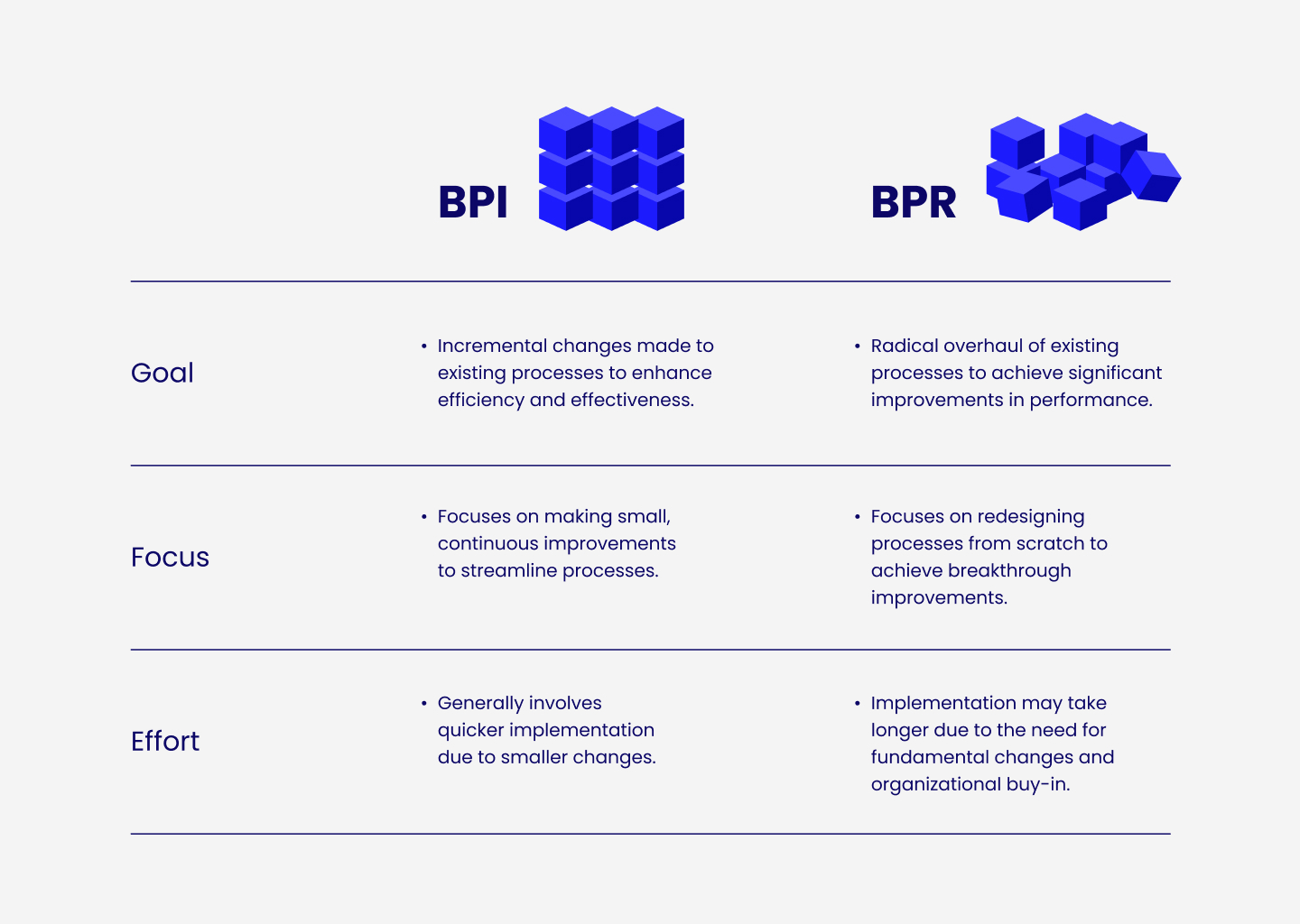

BPI vs. BPR

While BPI and BPR share some common objectives — improved efficiency and optimal resource utilization — they differ in some key areas. Here are three key aspects where BPI and BPR differ:

Level of Change

BPI is about continuously asking yourself, “How can we make this better?” even when there’s no urgency to change a process. The focus is to identify inefficiencies, bottlenecks, and areas of waste within your current processes. For example, if you’re an online retailer, BPI could involve streamlining your order fulfillment process to reduce delivery times or using a more robust CRM to improve client relationships.

BPR involves a complete overhaul. It’s like tearing down an entire house and building it from scratch. Suppose you’re a retail company that wants to improve delivery times. But instead of optimizing the order fulfillment process, you redesign the entire supply chain, from sourcing to delivery.

Be careful, though. Companies often overwhelm themselves by overestimating their capacity for change. It’s hard to determine if a process redesign is viable without understanding your capacity for change. As David Michels and Kevin Murphy explain in their HBR article:

The current business landscape is evolving so rapidly and unpredictably that executives are full of questions about change. How much? They want to know. How fast? How sustainable? And sometimes, just how? In our experience companies can’t hope to answer these questions unless they understand their own capacity for change.

Implementing BPI takes less time than implementing BPR. Think of BPI as a series of quick wins. You zoom into your process, find areas for improvement, make changes, and repeat. The exact time frame may differ based on the adjustments you want to make and could take weeks or months.

BPR is a marathon, not a race. It requires redesigning the process from scratch. A successful redesign might involve significant investments in technology and training. This requires careful consideration and meticulous execution. Naturally, redesigning and executing can take a long time, typically months or even years.

Risk and Disruption

There’s a significant divergence between BPI and BPR regarding risk and divergence. Since BPI involves making small changes, the level of disruption and risk is relatively lower.

Employees are less likely to resist these small changes because BPI builds on existing structures and practices. Plus, the changes are implemented gradually, so the transition is smoother and causes minimal disruption to your business’s day-to-day operations.

On the other hand, BPR involves challenging deeply ingrained practices and questioning conventions. Employees might have to step out of their comfort zone to execute changes of that magnitude, so there’s greater risk and disruption. Before you move forward with BPR, ensure that you and your team are prepared for that change.

We believe that most firms do not proactively manage change risk in a way that’s commensurate with the benefits of success and the costs of failure. Effectively managing change risk is a necessary ‘muscle’ to reduce, preempt, mitigate, and manage the challenges that come with (intents of) transformation, without bringing decision paralysis or stifling innovation in the organization.

Choosing between BPI and BPR is a crucial strategic decision. There are multiple factors to consider, such as:

Need for Change

What’s the current state of the process and its inefficiencies? Fundamentally flawed or outdated processes call for BPR. Eliminating fundamental flaws or updating your entire process with incremental changes can take a long time — not practical. However, BPI is a more suitable choice when the process is relatively sound but has some areas of inefficiency.

Suppose you’re a software development company. You’re struggling with lengthy approval cycles, siloed communication, and inconsistent quality standards because of an outdated development process. This warrants a complete process overhaul — you can’t afford to compromise on quality for long, can you?

Alignment With Strategy

Does the process align with your strategic goals? If a process no longer meets your business’s evolving needs or is preventing you from achieving your goals, it’s time to reengineer the process. Conversely, if your process is fundamentally aligned with your strategic objectives, but requires optimization to improve efficiency and customer satisfaction, BPI is the way to go.

For example, BPR is a better choice for an ecommerce company that wants to differentiate itself through personalized customer experiences and finds its current sales process rigid and transactional. But BPI makes more sense if the process is already customer-centric and requires additional personalization.

Risk Appetite

Assess your risk appetite before reengineering a process — can your business accept the disruption that comes with dismantling a key process and reimplementing it? For example, if a small manufacturer plans to transition from traditional batch production to lean manufacturing, the cost of implementing the new process and the halted production can translate to a major cost for the business.

Available Resources

BPI is less resource-intensive than BPR. Even when you’re running low on cash or don’t have the expertise to implement a radical shift in your process, you can make small improvements to your process over time.

Enhance Business Processes with Blanc Labs

Blanc Labs helps businesses like yours not only choose the right way forward but also offers comprehensive assistance to implement incremental changes strategically or re-engineer processes from scratch. If you need help navigating a change in business process, get in touch with us.

Insight | Banking Automation | IT Management | Nearshore IT Support

Canadian IT services firms offer a strategic opportunity for US Banks and FIs

January 29, 2024

In today’s challenging environment, U.S. bank IT departments are under unprecedented pressure to deliver more with limited resources. Cost-effective Canadian nearshore IT support, especially from technology-rich regions like Toronto, are emerging as a compelling opportunity for U.S. banks seeking to transform their technology infrastructure and enhance operational efficiency.

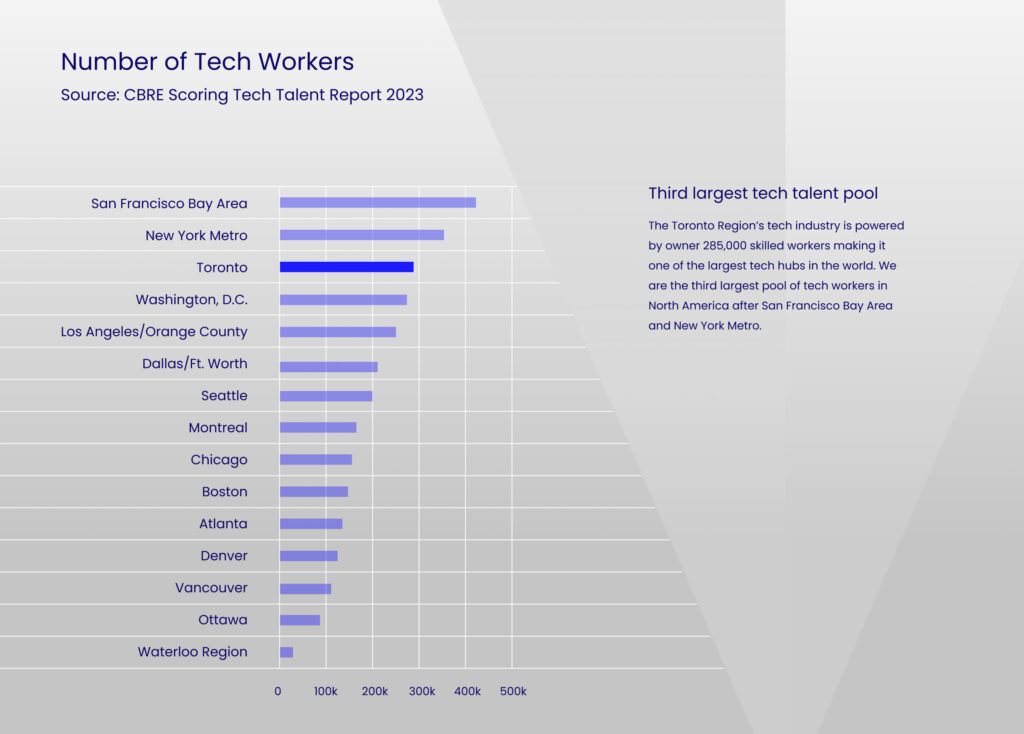

Toronto: Access to World-Class Technology Talent

Toronto is recognized globally as a Canadian center for technology and fintech companies. This world-class and fast growing city with 6.5 million citizens in 2023 is a dynamic and creative urban environment that at this point has become a self-sustaining financial technology hub, making it an ideal partner for U.S. banks seeking talent to drive their transformation roadmaps further and faster.

The region is home to top-tier universities like the University of Toronto, Waterloo and York University are renowned for their research and technology programs, providing a steady stream of skilled graduates and fostering a culture of innovation. Additionally, Toronto hosts the MaRS Discovery District, one of the world’s largest urban innovation hubs. MaRS provides a platform for tech start-ups and entrepreneurs, further solidifying Toronto’s status as a leader in technological development and innovation.

Proximity and Time Zone Alignment

Toronto’s geographical proximity, where almost any major U.S. city can be easily reached with a short, direct flight, offers significant benefits, including time zone alignment for real-time collaboration and agile project management. This is particularly advantageous compared to offshoring and other options. The ease of travel not only strengthens business relationships but also ensures effective communication and alignment, which are critical for the success of complex IT projects.

Cost-Effectiveness

Choosing Toronto for nearshore IT support allows U.S. banks to maintain high service standards while managing operational costs. The significant savings, often ranging from 30-50%, are a result of the current exchange rate differences between the U.S. and Canada, coupled with the inherent efficiencies in project management and execution. These financial benefits can be redirected towards other areas of growth and innovation.

Regulatory and Cultural Alignment

The U.S. and Canada share many regulatory and cultural similarities, which simplifies compliance standards and business practice alignment. This is vital for U.S. banks to minimize legal and operational risks in the highly regulated banking sector.

Customized and Scalable Solutions

Nearshore IT support in Toronto offers tailored, scalable solutions to meet specific banking needs. This flexibility ensures IT services adapt to the bank’s growth and changing priorities, promoting long-term sustainability. Moreover, these solutions are market-proven and highly relevant for U.S. banks, having been successfully implemented and delivering tangible results in similar banking environments.

Enhanced Security

Canadian nearshore IT support provides enhanced security, ensuring compliance with North American data protection laws. This safeguards sensitive information and customer data. Look for a SOC2 certification, which signifies a firm that can adapt to the stringent security requirements, a crucial aspect for U.S. banks in safeguarding their operations and customer information.

Looking for a Canadian tech partner? Let us help.

For U.S. banks striving to stay ahead in innovation, cost-effective Canadian nearshore IT support is a compelling strategic choice. Partnering with Toronto-based firms, such as Blanc Labs, maximizes these benefits, leading to improved efficiencies, fostering innovation, and enhancing customer satisfaction, significantly contributing to the bank’s success.

Les Riedl, Managing Principal of 10XBizDEV, is dedicated to connecting US Banks with innovative, best-in-class solutions and services that contribute to their success. His extensive experience as CEO and board member in fintech and financial services consulting provides valuable insights into the sector’s evolving challenges and opportunities. As US advisor for Blanc Labs, Les is instrumental in introducing their world-class capabilities to the American market.

Related Insights

Financial Services

Advisory Services

Digital Transformation for Lenders

Articles

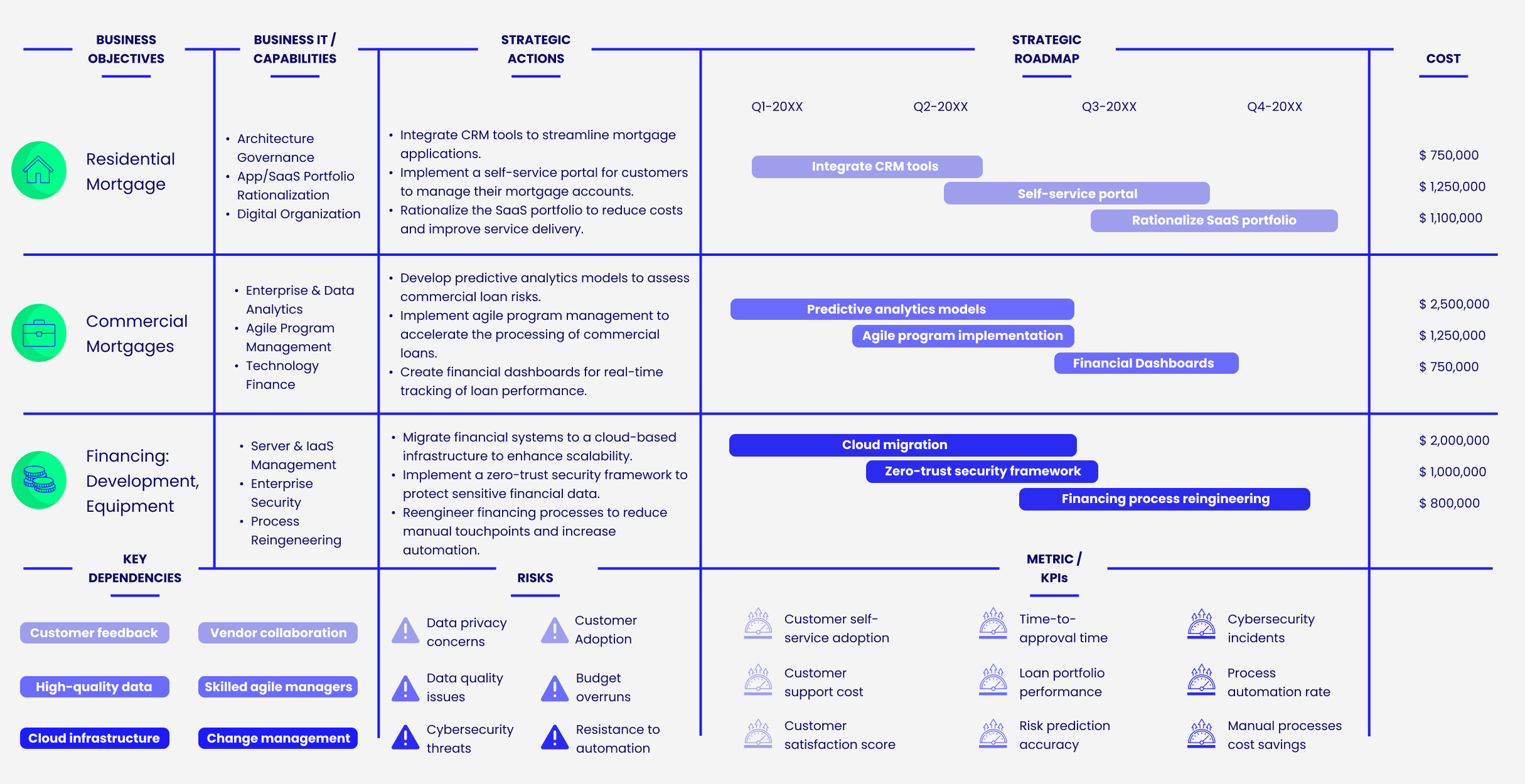

Lenders Transformation Playbook: Bridging Strategy and Execution

Mid-sized financial services institutions (FIs) are facing significant challenges during this period of rapid technological change, particularly with the rise of artificial intelligence (AI). As customer expectations grow, smaller banks and lenders must stay competitive and responsive. Canada’s largest financial institutions are already advancing in AI, while many others remain in ‘observer’ mode, hesitant to invest and experiment. Yet, mid-sized FIs that adopt the right strategy have unique agility, allowing them to adapt swiftly and efficiently to technological disruptions—even more so than their larger counterparts.

Trez distributes capital based on very specific criteria. But with over 300 investments in their portfolio, they process numerous payment requests and deal with documents in varied data formats. They saw an opportunity to enhance efficiency, improve task management, and better utilize data insights for strategic decision-making.

Blanc Labs and TCG Process have partnered to transform lending operations with innovative automation solutions, using the DocProStar platform to enhance efficiency, compliance, and customer satisfaction in the Canadian lending market.

Blanc Labs Partners with TCG Process to Integrate their Automation and Orchestration Platform and deliver Advanced Intelligent Workflow Automation to Financial Institutions

Blanc Labs and TCG Process have partnered to transform lending operations with innovative automation solutions, using the DocProStar platform to enhance efficiency, compliance, and customer satisfaction in the Canadian lending market.

Banking and financial services are changing fast. Moving from old, paper methods to new, digital ones is key to staying in business. It’s important to think about how business process improvement (BPI) can help.

A business process improvement specialist identifies bottlenecks and inefficiencies in your workflows, allowing you to focus efforts on automating the right processes.

We’ve developed this resource to help technical teams adopt an Open Banking approach by explaining a high-level solution architecture that is organization agnostic.

Explore the transformative influence of large language models (LLMs) on document processing in this insightful article. Discover how these cutting-edge models are reshaping traditional approaches, unlocking new possibilities in data analysis, and revolutionizing the way we interact with information.

Mid-sized financial services institutions (FIs) are facing significant challenges during this period of rapid technological change, particularly with the rise of artificial intelligence (AI). As customer expectations grow, smaller banks and lenders must stay competitive and responsive. Canada’s largest financial institutions are already advancing in AI, while many others remain in ‘observer’ mode, hesitant to invest and experiment. Yet, mid-sized FIs that adopt the right strategy have unique agility, allowing them to adapt swiftly and efficiently to technological disruptions—even more so than their larger counterparts.

Trez distributes capital based on very specific criteria. But with over 300 investments in their portfolio, they process numerous payment requests and deal with documents in varied data formats. They saw an opportunity to enhance efficiency, improve task management, and better utilize data insights for strategic decision-making.

Blanc Labs and TCG Process have partnered to transform lending operations with innovative automation solutions, using the DocProStar platform to enhance efficiency, compliance, and customer satisfaction in the Canadian lending market.

Blanc Labs Partners with TCG Process to Integrate their Automation and Orchestration Platform and deliver Advanced Intelligent Workflow Automation to Financial Institutions

Blanc Labs and TCG Process have partnered to transform lending operations with innovative automation solutions, using the DocProStar platform to enhance efficiency, compliance, and customer satisfaction in the Canadian lending market.

Banking and financial services are changing fast. Moving from old, paper methods to new, digital ones is key to staying in business. It’s important to think about how business process improvement (BPI) can help.

A business process improvement specialist identifies bottlenecks and inefficiencies in your workflows, allowing you to focus efforts on automating the right processes.

We’ve developed this resource to help technical teams adopt an Open Banking approach by explaining a high-level solution architecture that is organization agnostic.

Explore the transformative influence of large language models (LLMs) on document processing in this insightful article. Discover how these cutting-edge models are reshaping traditional approaches, unlocking new possibilities in data analysis, and revolutionizing the way we interact with information.

Mid-sized financial services institutions (FIs) are facing significant challenges during this period of rapid technological change, particularly with the rise of artificial intelligence (AI). As customer expectations grow, smaller banks and lenders must stay competitive and responsive. Canada’s largest financial institutions are already advancing in AI, while many others remain in ‘observer’ mode, hesitant to invest and experiment. Yet, mid-sized FIs that adopt the right strategy have unique agility, allowing them to adapt swiftly and efficiently to technological disruptions—even more so than their larger counterparts.

Trez distributes capital based on very specific criteria. But with over 300 investments in their portfolio, they process numerous payment requests and deal with documents in varied data formats. They saw an opportunity to enhance efficiency, improve task management, and better utilize data insights for strategic decision-making.

Blanc Labs and TCG Process have partnered to transform lending operations with innovative automation solutions, using the DocProStar platform to enhance efficiency, compliance, and customer satisfaction in the Canadian lending market.

Blanc Labs Partners with TCG Process to Integrate their Automation and Orchestration Platform and deliver Advanced Intelligent Workflow Automation to Financial Institutions

Blanc Labs and TCG Process have partnered to transform lending operations with innovative automation solutions, using the DocProStar platform to enhance efficiency, compliance, and customer satisfaction in the Canadian lending market.

Banking and financial services are changing fast. Moving from old, paper methods to new, digital ones is key to staying in business. It’s important to think about how business process improvement (BPI) can help.

A business process improvement specialist identifies bottlenecks and inefficiencies in your workflows, allowing you to focus efforts on automating the right processes.

We’ve developed this resource to help technical teams adopt an Open Banking approach by explaining a high-level solution architecture that is organization agnostic.

Explore the transformative influence of large language models (LLMs) on document processing in this insightful article. Discover how these cutting-edge models are reshaping traditional approaches, unlocking new possibilities in data analysis, and revolutionizing the way we interact with information.

Financial Services | AI | Banking Automation | Digital Banking | Enterprise Automation

Using RPA in Banking

May 8, 2023

All banking or financial institutions can relate to the struggle of managing piles of structured and unstructured data daily. This task requires repetitive and manual effort from your employees that they could otherwise dedicate to high-value work. It can also be time-consuming and prone to errors, ultimately hampering your bank’s customer experience. Fortunately, automation technologies are proving to be a boon for the finance sector.

The finance domain is experiencing a major transformation, with banking automation and digitization at the forefront. According to a study by McKinsey, machines will handle between 10% to 25% of banking functions in the next few years, which can free up valuable time and resources for employees to focus on more strategic initiatives.

What is Robotic Process Automation (RPA)?

RPA is an automation technology governed by structured inputs and business logic. RPA in banking is a powerful tool that can automate repetitive and time-consuming tasks. It allows banks and financial institutions to gain a competitive advantage by automating routine tasks cost-effectively, fast, and without errors.

Banks, credit unions, or other financial institutions can set up robotic applications to handle tasks like capturing and analyzing information from documents, performing transactions, triggering responses, managing data, and coordinating with other digital systems. The possibilities for using RPA in finance are innumerable and can include a range of functionalities such as generating reports, sending auto emails, and even auto-decisioning.

How RPA works

Robotic Process Automation works by automating repetitive and routine tasks that are currently performed manually. Software robots, also known as ‘bots,’ are designed to mimic human actions and interactions with digital systems. These rule-based bots can be configured to perform specific tasks, such as document processing, data entry, transaction execution, complete keystrokes, and more.

Once a bot is configured, it can be triggered to run automatically or on a schedule, freeing up human resources to focus on customer service or other higher-value or strategic activities. The bot interacts with the relevant systems and applications, capturing and analyzing data, navigating systems, and automating workflows as needed.

One of the key advantages of RPA in finance is that it is non-intrusive, meaning that it operates within existing systems and processes, without requiring any changes to the underlying infrastructure. This means that no changes are made to the underlying applications. RPA bots perform tasks in a similar manner to employees- by signing into applications, entering data, conducting calculations, and logging out. They do this at the user interface or application surface layer by imitating mouse movements and the keystrokes made by employees.

This makes it easier to implement and reduces the risk of disruption to existing operations. As per Forbes, RPA usage has seen a rise in popularity in the last few years and will continue to see double-digit growth in 2023.Many people use the terms ‘RPA’ and ‘Intelligent Automation’ (IA) interchangeably. Both are banking automation technologies that improve efficiency, but are they the same?

Are RPA and Intelligent Automation the same?

No, RPA is not IA and IA is not RPA. While RPA is a rule-based approach for everyday tasks, intelligent automation uses Artificial Intelligence (AI) and Machine Learning (ML) technologies to automate more complex and strategic processes. IA encompasses a wide range of technologies which includes RPA. IA enables organizations to automate not just manual tasks but also decision-making processes and allows for continuous improvement through self-learning.

A combination of IA and RPA can unlock the true potential of banking automation. When RPA is combined with the powers of AI, ML, and natural language processing, it dramatically increases the software’s skills to execute advanced cognitive processes like understanding speech, carrying out conversations, comprehending semi-structured tasks such as purchase orders, invoices and unstructured documents like emails, text files and images.

Thus, RPA and its combination technologies are fully capable of taking your banking and financial business to new heights.

What are the benefits of RPA in Banking?

The global RPA market is projected to grow at a CAGR of 23.4%, from $10.01 Billion in 2022 to $43.2 Billion in 2029. Evidently, more industries worldwide are realizing the importance of RPA. Here are some benefits of using RPA in banking and financial institutions.

Improved Scalability

Robots can work faster and longer than humans without taking breaks. RPA can also be scaled to meet changing business needs, making it an ideal solution for organizations that are looking to grow and expand their operations and provide additional services.

Enhanced Compliance and Risk Management

RPA can help banks and financial institutions improve their compliance and risk management processes. For example, the software can be configured to monitor transactions for potential fraud and to ensure compliance with regulatory requirements. It can also inform the bank authorities in case any anomaly is found.

Improved Customer Service

RPA can enable faster and more personalized service to customers. For example, the software can be configured to handle routine customer inquiries and transactions, reduce wait times and improving the overall customer experience.

Increased Efficiency

RPA can automate repetitive and manual tasks, redirecting human resources to other higher-value and strategic activities. This can result in faster processing times, improved accuracy, and reduced costs. According to a study by Deloitte, banking institutions could save about $40 million over the first 3 years of using RPA in banking.

Better Data Management

RPA can automate the collection, analysis, and management of data, making it easier for banks and financial institutions to gain insights and make informed decisions. This means faster account opening or closing, loan and document processing, data entry, and retrieval.

Top Use Cases of RPA in Banking

RPA can be applied in several ways in the banking and finance industry. Here are some examples of RPA use cases in banking and finance:

Accounts Payable

RPA can automate the manual, repetitive tasks involved in the accounts payable process, such as vendor invoice processing, field validation, and payment authorization. RPA software in combination with Optical Character Recognition (OCR) can be configured to extract data from invoices, perform data validation, and generate payment requests, reducing the risk of errors and freeing up human resources. This system can also notify the bank in case of any errors.

Mortgage Processing

Mortgage processing involves hundreds of documents that need to be gathered and assessed. RPA can streamline the mortgage application process by automating tasks such as document verification, credit checks, and loan underwriting. By using RPA to handle routine tasks, banks, and financial institutions can improve processing time, reduce the risk of errors, and enhance the overall customer experience.

Fraud Detection

According to the Federal Trade Comission (FTC), banks face the ultimate risk of forgoing money to fraud, which costs them almost $8.8 billion in revenue in 2022. This figure was 30% more than than what was lost to bank fraud in 2021 . RPA can assist in detecting potential fraud by automating the monitoring of transactions for unusual patterns and anomalies. Bots can be configured to perform real-time ‘if-then’ analysis of transaction data, flagging potential fraud cases as defined for further investigation by human analysts.

KYC (Know Your Customer)

RPA can automate the KYC onboarding process, including the collection, verification, and analysis of customer data. RPA software can be configured to handle routine tasks such as data entry, document verification, and background checks, reducing the risk of errors and faster account opening, thus resulting in enhanced customer satisfaction.

Thus, using RPA in your bank and financial institution can not only save time and money but also boost productivity. Banking automation gives you a chance to gain a competitive edge by leveraging technology and becoming more efficient.

Blanc Labs Automation Solution for Banks

Blanc Labs helps banks, credit unions, and financial institutions with their digital transformation journey by providing solutions that are RPA-based. Our services include integrating advanced automation technologies into your processes to boost efficiency and reduce the potential for errors caused by manual effort.

We offer a tailored approach that combines RPA, ML, and AI to automate complex tasks, such as mortgage processing and document processing, allowing you to conserve resources, speed up decision-making and provide quicker and improved financial services to your customers.

If your bank processes a huge amount of data everyday, we can help you. Book a discovery call with us and let us explain how we can increase the efficiency of your bank’s core functions. Our team will analyze your current processes and propose a tailor-made automation solution that can operate seamlessly and in conjunction with your existing systems.

Financial Services | AI | Banking Automation | Digital Banking | Lending Technology

How to Automate Loan Origination Systems

May 1, 2023

Loan origination automation is critical because the loan origination process is labor-intensive and prone to human error.

Translation?

The process takes expensive human capital that you can dedicate to other, more strategic tasks. It’s also prone to human error, which increases your costs and puts your reputation at risk.

Automating the process takes humans out of the equation, minimizing the cost of human capital and the risk of human error.

In this article, we explain how to automate the process using an automated loan origination system.

What is the Loan Origination Process?

Loan origination is the process of receiving a mortgage application from a borrower, underwriting the application, and releasing the funds to the borrower or rejecting the application.

When a customer applies for a mortgage, the lender initiates (or originates) the process necessary to determine if a borrower should be lent funds according to the institution’s policies.

The process is extensive and takes an average of 35 to 40 days. The origination process involves five steps, as explained below.

Prequalification

Prequalification is a screening stage. This is where lenders look for potential reasons that can adversely impact a borrower’s capability to repay the loan.

Typically, lenders look for things like:

Income: Does the borrower make enough money to be able to service the loan payments, and is that income consistent?

Assets: Should the borrower’s income stop for some reason; do they have enough assets to remain solvent given their existing liabilities?

Debt: Is the borrower overleveraged? Are the debts secured or unsecured?

Credit record: Has the buyer made loan payments on time in the past?

These factors help the lender determine if they should spend time processing the application further.

Preparing a Loan Packet

Lenders create a packet (essentially a file of documents) for prequalified borrowers.

The packet includes the borrower’s documents, including KYC, financial statements, and other relevant documents that provide an overview of the borrower’s debt servicing capability.

Lenders also include documents that highlight the reasons that make an applicant eligible or ineligible to be considered for the loan.

For example, the lender may include the borrower’s debt-to-income ratio, properties and assets at market value, and income streams to provide an overview of whether the borrower is a good candidate for the loan.

Some lenders take extra steps to double-check the applicant’s claims.

For example, lenders might hire a valuer or research property rates to verify your real estate investment’s current market value. The valuer’s report is added to the packet for the underwriter’s reference.

Negotiation

Many borrowers, especially those with an excellent credit record, browse their options before accepting a lender’s offer.

The borrower might want to negotiate a lower rate or ask for a fixed rate instead of a floating rate.

Term Sheet Disclosure

A term sheet is a summary of the loan. It’s a non-binding document that contains the terms and conditions of the mortgage deal.

The term sheet includes the tenure, interest rate, principal amount, foreclosure charges, processing fees, and other relevant details.

Loan Closing

If the negotiations go well and the borrower accepts the offer, the lender closes the loan.

The lender creates various closing documents, including final closing disclosure, titling documents, and a promissory note.

The borrower and lender sign the documents, and the lender disburses the funds as agreed.

3 Ways to Automate Loan Origination

Now that you know the loan origination process, let’s talk about automating parts of this process to make it more efficient.

Digitizing Loan Applications

You can create an online portal where applicants can initiate a loan application and upload their KYC and other documents.

The documents are automatically transferred to your internal systems for prequalifying the applicant.

IDP extracts and relays the applicant’s data from the documents to your system.

Once the data is in the system, robotic process automation (RPA) can be used to determine if an applicant should be prequalified.

You can use a machine learning (ML) algorithm for deeper insights.

ML can help identify characteristics that make a person more or less likely to service the loan until the end of the term, allowing you to make smarter decisions.

Assembling Loan Documentation

Cloud-based RPA can collect documents from the online portal and organize them in one location. Not only are digital copies faster to collect, but they’re easy to store and search.

Think about it. You’ve received an application, but it’s missing the cash flow statement for last year. You’ll need to email or call the applicant to upload the documents, wasting your and the applicant’s time.

Lenders typically have a document checklist. Automating checklists is easy with RPA — when the applicant forgets to upload a document, the RPA can trigger notifications to the applicant.

The system can also notify the loan officer if the applicant becomes non-responsive.

Speeding Up Underwriting

Borrowers want faster access to funds, but lenders must complete their due diligence.

Lending automation can help reduce the time between application and approval.

With technologies like artificial intelligence (AI), ML, and RPA, automation systems can assess an applicant’s creditworthiness within seconds.

RPA can help with basics like checking the minimum credit score and income levels. RPA can also flag any areas that indicate greater risk, such as excessive variability in the applicant’s cash flows.

Moreover, loan origination is a compliance-heavy process. It’s easy to forget a small step when you’re overwhelmed with loan applications.

RPA ensures all compliance steps are taken care of. If they’re not, the system can trigger alerts for the underwriter as well as the superiors.

AI and ML can provide deeper insights. These technologies can use big data to identify patterns that make a borrower more likely to default, allowing you to make smarter decisions fast.

Moreover, AI and ML can help you look beyond credit scores and find people that are more creditworthy than their credit scores suggest.

As Dimuthu Ratnadiwakara, assistant professor of finance at Louisiana State University, explains:

“Traditional models tend to lock anyone with a low credit score—including many young people, college-educated people, low-income people, Black and Hispanic people and anyone who lives in an area where there are more minorities, renters and foreign-born—out of the credit market.”

How Shortening Loan Origination With Automation Helps

Shortening the loan origination process benefits you in multiple ways:

Match customer expectations: You’ll deliver on the customers’ expectations by offering faster loan processing. 40% of mortgage customers are willing to complete the entire process using self-serve digital tools, but 67% still interact with a human representative via phone.

Deliver better experiences: Automation offers various opportunities to improve customer experience. For example, you can set up an AI chatbot that responds to customers’ questions in real time.

Increase efficiency: You can process more applications per month by automating loan origination.

Better use of your staff’s time: Automated workflows allow credit officers to focus on parts of the business that require a human touch, such as building stronger relationships with clients, than on repetitive tasks that automation can perform more accurately.

Loan Origination Automation with Blanc Labs

Selecting the right partner to set up loan origination automation is critical. Partnering with Blanc Labs ensures frictionless implementation of a personalized loan origination system.

Blanc Labs tailor-makes solutions best suited for your needs and workflow. Blanc Labs starts by assessing your needs and creating a strategy to streamline your loan origination processes. Then, Blanc Labs creates an automation system using technologies like RPA, AI, and ML.

Book a demo to learn how Blanc Labs can help you automate your loan origination workflow.

Financial Services | AI | Banking Automation | Digital Transformation | Enterprise Automation

10 Tips to Successfully Implement RPA in Finance

April 14, 2023

Automation has taken the finance industry by storm, and for all good reasons. Banking automation technologies like Robotic Process Automation (RPA) come with the promise of streamlining processes and increasing efficiency.

According to Forbes, RPA has the potential to transform the way finance functions, from reducing manual errors to freeing up valuable resources. To help you maximize the benefits of RPA in finance, we’ve put together a list of 10 tips for successful implementation. But first, let’s take a step back and explore what RPA is.

What is Robotic Process Automation (RPA)?

RPA is the use of software robots to automate routine and repetitive tasks like document processing, freeing up employees to focus on strategic activities that can lead to better customer service or innovations that could meet customer expectations.

The bots are programmed to follow specific rules and procedures to complete a task, just like an employee. They can interact with various software applications and systems, such as spreadsheets and databases, to collect and process data. The bots can also make decisions, trigger responses, and communicate with other systems and software.

When a task is triggered, the bot performs it automatically, eradicating the scope of errors that may be produced through manual processes. The process is monitored and managed by a central control system, allowing adjustments and updates to be made as needed.

Think of RPA as a digital workforce, working tirelessly in the background to complete tasks that would otherwise take hours to complete. With RPA in finance, your financial institution can increase efficiency, reduce costs, and improve the accuracy of its processes.

The Use of RPA in Banking Automation

There are many ways in which RPA can be used in banking automation. Here are some of them:

Customer Service Automation

RPA is capable of automating routine customer service tasks such as account opening, balance inquiries, and transaction processing, allowing bank employees to focus on more complex customer needs.

Loan Processing

RPA in banking and finance can streamline the loan processing workflow by automating repetitive tasks such as document collection and verification, credit score analysis, and loan decision-making.

Fraud Detection and Prevention

In 2022 alone, banks and financial institutions lost $500K to fraud. Technologies like RPA can analyze vast amounts of data to detect and prevent fraud in real-time, improving the accuracy and speed of fraud detection. It may also report any suspected fraud to the banking authorities as soon as it is discovered.

KYC and AML Compliance

Verification and compliance document processing can eat up a major share of your institution’s resources. RPA can automate the process of collecting, verifying, and analyzing customer information, helping banks to comply with KYC (Know Your Customer) and AML (Anti-Money Laundering) regulations.

Back Office Operations

RPA can automate various back-office tasks such as data entry, reconciliation, report generation, monthly closing, and management reports, freeing up employees to focus on more strategic initiatives.

Payment Processing

Manual data entry in payment processing can lead to manual errors and longer processing time. RPA can automate the payment processing workflow, including payment initiation, authorization, and settlement, reducing the risk of errors and improving efficiency.

Risk Management

Banks and financial institutions are constantly at risk from various sources. RPA in finance can help institutions identify, assess, and manage risks by automating data collection, analysis, and reporting, improving the accuracy and speed of risk assessments.

Internal Compliance Monitoring

RPA can automate the process of monitoring and reporting on compliance with internal policies and regulations, reducing the risk of non-compliance and improving overall compliance management.

The potential of RPA in banking and finance is unlimited. When combined with Intelligent Automation technologies, RPA can leverage Artificial Intelligence (AI) and Machine Learning (ML) to provide more intelligent process automation. While the technology in itself is efficient, financial institutions must know how to implement it for maximized benefit.

10 Tips for Successfully Implementing RPA in Finance

According to the Deloitte Global RPA survey, 53% of organizations who took part in the survey have already begun their RPA implementation. The number is expected to rise to 72% over the next year. Entering the RPA race can be quick, but managing and scaling it is a different ball game. Before getting started with automation initiatives, it is important to consider the following tips.

Start Small

While RPA might seem useful to rejuvenate all of your systems and processing, it is important to consider the business impact and start small. Beginning with a smaller project, for example, a single process or department can help build momentum and demonstrate the benefits of RPA. It also allows the organization to gain experience and develop a better understanding of the technology before scaling up.

Define Clear Goals

The key to successful RPA implementation rests in your goals. Decide what you want to achieve with RPA in consultation with your IT department. Having a clear understanding of the goals and objectives of the RPA implementation will ensure that resources are allocated appropriately and that the project stays on track. Aim for specific, measurable, achievable, relevant, and time-bound (SMART) goals.

Involve Stakeholders

Engaging stakeholders, such as the management, finance employees, and IT, can help build better design and smoother change management for the RPA implementation. It also ensures that the RPA system is well-integrated across departments and addresses the needs and concerns of all stakeholders.

Assess Processes

When a financial institution leverages too many bots to automate processes, it results in a pile of data. They may be tempted to use ML on the data and create a chatbot to make customer queries easier. However, it can lead to a poorly planned ML project. Thus, a thorough assessment of the processes is critical to ensure that the RPA implementation does not get sidetracked. This assessment should include an analysis of the tasks, inputs, outputs, and stakeholders involved in the process.

Choose the Right Tools

Selecting the right RPA tools and technology is critical to the success of the implementation. Decide the mix of automation technologies your institution requires before reaching out to a vendor. Factors to consider include the cost, scalability, and ease of use , as well as its ability to integrate with other systems and applications.

Define Roles and Responsibilities

Clearly defining the roles and responsibilities of the RPA team, including project governance, testers, and users, is important to ensure that everyone knows what is expected of them. Remember that automation is a gradual process, and your employees will still need to interfere if it is not properly automated.

Ensure Data Security

Protecting sensitive data and customer information is a key concern in finance. RPA needs to be implemented in such a way that data security remains unaffected. Discuss with your vendor about strong security measures to ensure that data is protected and that the confidentiality of customer information is maintained.

Plan for Scalability

There are thousands of processes in banks and financial institutions that can use automation. Thus, the RPA implementation should be planned with scalability in mind so that the technology and processes can be scaled up as needed. This helps to ensure that the RPA can be combined with AI and ML technologies as necessary and the implementation remains relevant in the long term.

Monitor and Evaluate Performance

Continuously monitoring and evaluating the performance of the RPA bots is critical to ensure that they are operating effectively and efficiently. Also, do not forget to keep HR in the loop so that employees are informed and trained about the changing processes and how to use them in a timely manner. Regular evaluations should be conducted to identify areas for improvement and to make adjustments as needed.

Foster a Culture of Innovation

Encouraging a culture of innovation and experimentation can help to ensure that the organization is prepared for the future. Consult your IT department and automate your entire development lifecycle to protect your bots from disappearing after a major update. Invest in a center of excellence that can create business cases, measure ROI and cost optimization and track progress against goals.

Implementation Automation with Blanc Labs

At Blanc Labs, we understand that every financial and banking institution has unique needs and challenges when it comes to RPA implementation. That’s why we offer tailor-made RPA solutions to ensure seamless implementation for our clients.

Our RPA systems are designed to be flexible and scalable, allowing our clients to start small and grow as needed. We provide end-to-end support, from process assessment and design to implementation and ongoing assistance, to ensure that our clients realize the full benefits of RPA.

Booking a free consultation with us is the first step toward successful RPA implementation. Our team of experts work closely with each client to understand their specific requirements and goals to build a customized RPA solution to meet their needs.

Financial Services | AI | Banking Automation | Gen AI | ML

Banking Automation: The Complete Guide

April 6, 2023

Banks are process-driven organizations. Processes ensure accuracy and consistency across the organization. They are also repetitive. Over the past decade, the transition to digital systems has helped speed up and minimize repetitive tasks. But to prepare yourself for your customers’ growing expectations, increase scalability, and stay competitive, you need a complete banking automation solution.

Systems powered by artificial intelligence (AI) and robotic process automation (RPA) can help automate repetitive tasks, minimize human error, detect fraud, and more, at scale. You can deploy these technologies across various functions, from customer service to marketing.

Many, if not all banks and credit unions, have introduced some form of automation into their operations. According to McKinsey, the potential value of AI and analytics for global banking could reach as high as $1 trillion.

If you are curious about how you can become an AI-first bank, this guide explains how you can use banking automation to transform and prepare your processes for the future.

What is Banking Automation?

Banking automation involves automating tasks that previously required manual effort.

For example, banks have conventionally required staff to check KYC documents manually. However, banking automation helps automatically scan and store KYC documents without manual intervention.

Cost saving is generally one of RPA’s biggest advantages.

According to a Gartner report, 80% of finance leaders have implemented or plan to implement RPA initiatives.

The report highlights how RPA can lower your costs considerably in various ways. For example, RPA costs roughly a third of an offshore employee and a fifth of an onshore employee.

You can make automation solutions even more intelligent by using RPA capabilities with technologies like AI, machine learning (ML), and natural language processing (NLP). According to a McKinsey study, AI offers 50% incremental value over other analytics techniques for the banking industry.

With that in mind, let’s look closely at RPA and how it works.

Generative AI and Banking Automation

The latest trend in banking automation is the use of Generative AI.

Retail banking and wealth: Generative AI can create more accurate NLP models and help automated systems process KYC documents and open accounts faster.

SMB banking: Generative AI can help interpret non-numeric data, like business plans, more effectively.

Commercial banking: Generative AI will enable customers to get answers about financial performance in complex scenarios.

Investing banking and capital markets: Banks could use generative AI to stress test balance sheets with complex and illiquid assets.

Banks are already using generative AI for financial reporting analysis & insight generation. According to Deloitte, some emerging banking areas where generative AI will play a key role include fraud simulation & detection and tax and compliance audit & scenario testing.

What is RPA?

Robotic process automation, or RPA, is a technology that performs actions generally performed by humans manually or with digital tools.

Say you have a customer onboarding form in your banking software. You must fill it out each time a customer opens an account. You’re manually performing a task using a digital tool.

RPA can perform this task without human effort. The difference? RPA does it more accurately and tirelessly—software robots don’t need eight hours of sleep or coffee breaks.

You can implement RPA quickly, even on legacy systems that lack APIs or virtual desktop infrastructures (VDIs).

Implementing RPA can help improve employee satisfaction and productivity by eliminating the need to work on repetitive tasks.

You can use RPA in banking operations for various purposes.

For example, Credigy, a multinational financial organization, has an extensive due diligence process for consumer loans.

The process was prone to errors and time-consuming. The company decided to implement RPA and automate the entire process, saving their staff and business partners plenty of time to focus on other, more valuable opportunities.

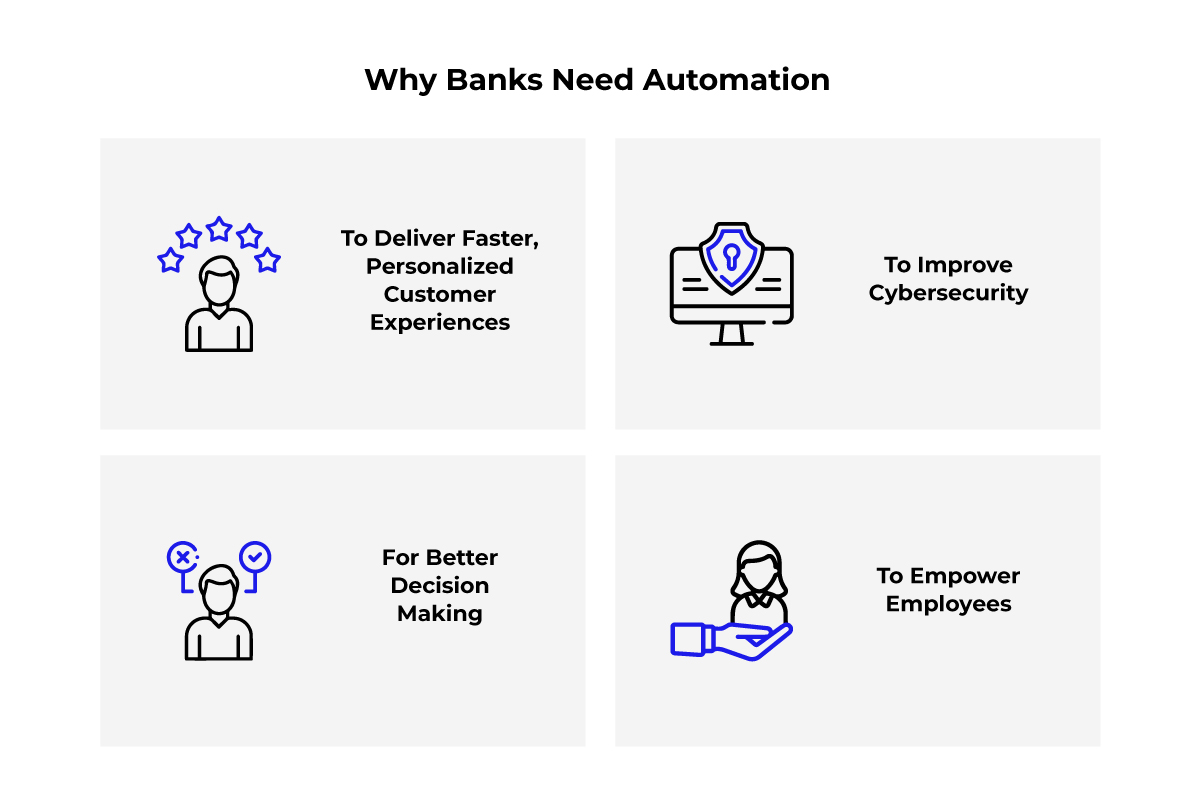

The Need for Automation in Banking Operations

Banks need automation to:

Deliver better customer experiences

Increase online security

Improve decision making

Empowering employees

Below, are more reasons for your bank to automate operations.

To Deliver Faster, Personalized Customer Experiences

New-gen customers want banks that can provide fast financial services online.

Thanks to the pandemic, the shift to digital has picked up pace. A digital portal for banking is almost a non-negotiable requirement for most bank customers.

In fact, 70% of Bank of America clients engage with the bank digitally. The bank’s newsroom reported that a whopping 7 million Bank of America customers used Erica, its chatbot, for the first time during the pandemic.

A chatbot can provide personalized support to your customers. A level 3 AI chatbot can collect the required information from prospects that inquire about your bank’s services and offer personalized solutions.

A chatbot is a great way for customers to get answers, but it’s also an excellent way to minimize traffic for your support desk.

To Improve Cybersecurity

Cybersecurity is expensive but is also the #1 risk for global banks according to EY. The survey found that cyber controls are the top priority for boosting operation resilience according to 65% of Chief Risk Officers (CROs) who responded to the survey.

Using automation to create a cybersecurity framework and identity protection protocols can help differentiate your bank and potentially increase revenue. You can get more business from high-value individual accounts and accounts of large companies that expect banks to have a top-notch security framework.

Automating cybersecurity helps take remedial actions faster. For example, the automated system can freeze compromised accounts in seconds and help fast-track fraud investigations.

Of course, you don’t need to implement that automation system overnight. With cloud computing, you can start cybersecurity automation with a few priority accounts and scale over time.

For Better Decision Making

AI and ML algorithms can use data to provide deep insights into your client’s preferences, needs, and behavior patterns.

These insights can improve decision-making across the board. For example, using these insights in your marketing strategy can help hyper-target marketing campaigns and improve returns.

Moreover, these insights help deliver greater value to customers. By making faster and smarter decisions, you’ll be able to respond to customers’ fast-evolving needs with speed and precision.

As a McKinsey article explains, banks that use ML to decide in real-time the best way to engage with customers can increase value in the following ways:

Stronger customer acquisition: Automation and advanced analytics help improve customer experience. They help personalize marketing across the customer acquisition journey, which can improve conversions.

Higher customer lifetime value: You can increase lifetime value by consistently engaging with customers to strengthen relationships across products and services.

Lower credit risk: Banks can screen customers by analyzing behavior patterns that signal higher default or fraud risk.

To Empower Employees

As you digitize banking processes, you’ll need to train employees. Reskilling employees allows them to use automation technologies effectively, making their job easier.

Your employees will have more time to focus on more strategic tasks by automating the mundane ones. This results in increased employee satisfaction and retention and allows them to focus on things that contribute to your topline — such as building customer relationships, innovating processes, and brainstorming ways to address customers’ most pressing issues.

Challenges Faced by Banks Today

Here are some key challenges that banks face today and how automation can help address them:

Inefficient Manual Processes

Manual processes are time and resource-intensive.

According to the 2021 AML Banking Survey, relying on manual processes hampers a financial organization’s revenue-generating ability and exposes them to unnecessary risk.

The simplest banking processes (like opening a new account) require multiple staff members to invest time. Moreover, the process generates paperwork you’ll need to store for compliance.

While you complete the account opening process, the customer is on standby, waiting to start using their account.

The slow service doesn’t exactly make a great impression. Customers want to be able to start using their accounts faster. If you’re too slow, they’ll find a bank that offers faster service.

Automation helps shorten the time between account application and access. But that’s just one of the processes that automation can speed up.

Technologies like RPA and AI can help fast-track processes across departments, including accounting, customer support, and marketing.

Automation Without Integration

Banks often implement multiple solutions to automate processes. However, often, these systems don’t integrate with other systems.

For end-to-end automation, each process must relay the output to another system so the following process can use it as input.

For example, you can automate KYC verification. But after verification, you also need to store these records in a database and link them with a new customer account. For this, your internal systems need to be integrated.

Connecting banking systems requires APIs. Think of APIs as translators. They help two software solutions communicate with each other. A system can relay output to another system through an API, enabling end-to-end process automation.

Increase in Competition

Canadians want more competition in banking. The competition in banking will become fiercer over the next few years as the regulations become more accommodating of innovative fintech firms and open banking is introduced.

An increase in competition will give customers more power. They’ll demand better service, 24×7 availability, and faster response times.

You’ll need automation to achieve these objectives and make yourself stand out in the crowd.

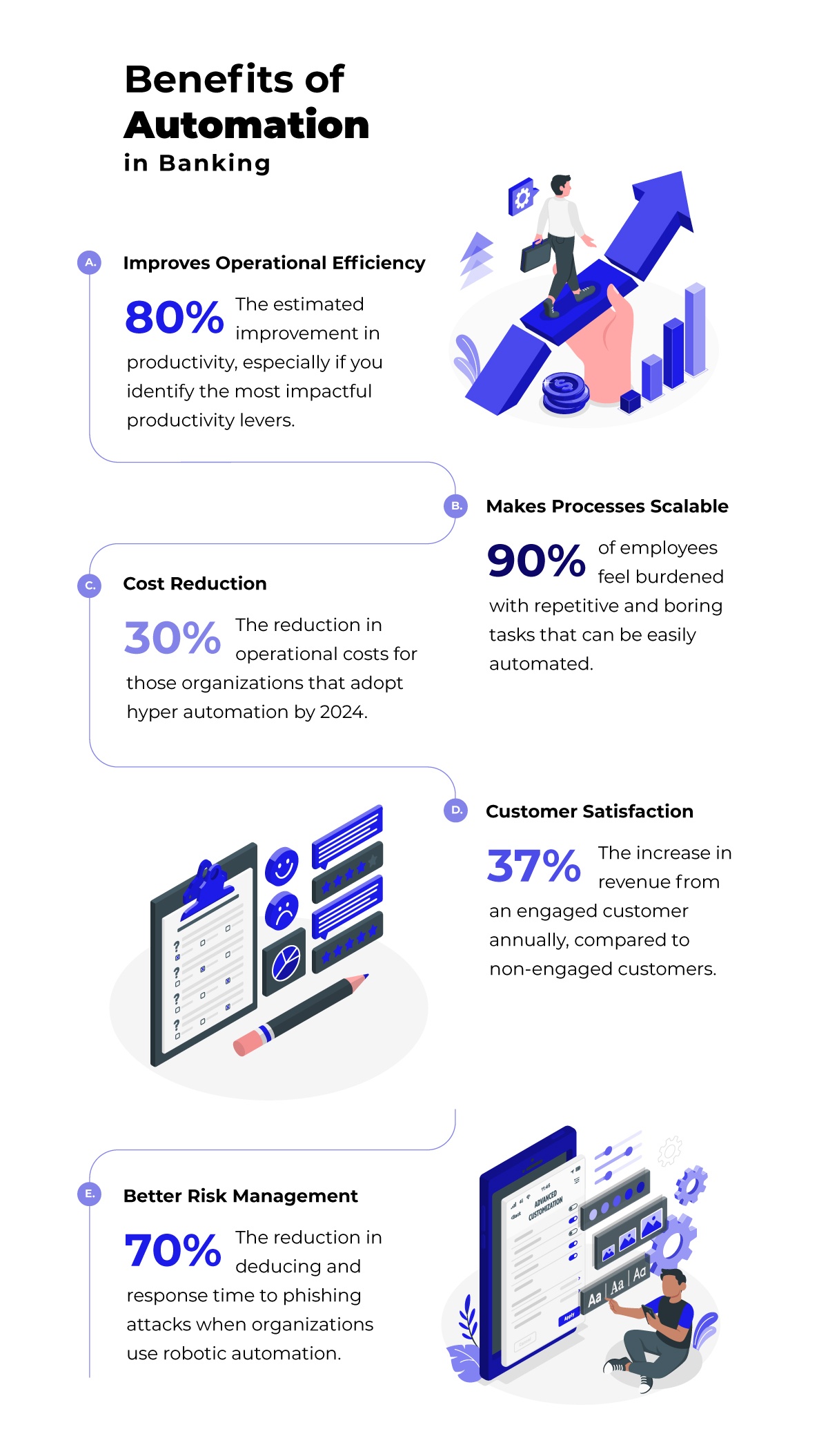

Benefits of Automation in Banking

Once you invest in automation, you can expect to derive the following benefits:

Improves Operational Efficiency

An error-free automation system can supercharge operational efficiency.

You’ll have to spend little to no time performing or monitoring the process. Moreover, you’ll notice fewer errors since the risk of human error is minimal when you’re using an automated system.

Implementing automation allows you to operate legacy and new systems more resiliently by automating across your system infrastructure. This increases efficiency, consistency, and speed.

Makes Processes Scalable

Banks noticed how automation could be an excellent investment during the pandemic. As explained in a World Economic Forum (WEF) article:

“Through the combination of a distinct data element with robotics process automation, it is possible to generate client documentation from management tools and archives at a high frequency. Due to its scalability, high volumes can be managed more efficiently.”

The article provides the example of Swiss banks. During the pandemic, Swiss banks like UBS used credit robots to support the credit processing staff in approving requests. The support from robots helped UBS process over 24,000 applications in 24-hour operating mode.

80% of banks still favor some form of print statements. The cost of paper used for these statements can translate to a significant amount. Automation and digitization can eliminate the need to spend paper and store physical documents.

b. Human error

Human error can require reworks and cause delays in processing customer requests. Errors can result in direct losses (like a lost sale) and indirect losses (like a lost reputation). Minimizing errors can help reduce the cost associated with human error.

c. Increased employee satisfaction

You’ll spend less per unit with more productive employees. Automation can help improve employee satisfaction levels by allowing them to focus on their core duties.

For example, a sales rep might want to grow by exploring new sales techniques and planning campaigns. They can focus on these tasks once you automate processes like preparing quotes and sales reports.

Working on non-value-adding tasks like preparing a quote can make employees feel disengaged. When you automate these tasks, employees find work more fulfilling and are generally happier since they can focus on what they do best.

As Professor Sgroi explains, “The driving force seems to be that happier workers use the time they have more effectively, increasing the pace at which they can work without sacrificing quality.”

Customer Satisfaction

Automation can help meet customer expectations in various ways.

Speed is one of the most difficult expectations to meet for banks. You want to offer faster service but must also complete due diligence processes to stay compliant. That’s where automation helps.

61% of customers feel a quick resolution is vital to customer service. As a bank, you need to be able to answer your customers’ questions fast.

How fast? Ideally, in real-time.

A level 3 AI chatbot can help provide real-time, personalized responses to your customers’ questions.

In addition to real-time support, modern customers also demand fast service. For example, customers should be able to open a bank account fast once they submit the documents. You can achieve this by automating document processing and KYC verification.

Better Risk Management

Automation can help minimize operational, compliance, and fraud risk.

Since little to no manual effort is involved in an automated system, your operations will almost always run error-free.

You can also automate compliance processes. For example, you can add validation checkpoints to ensure the system catches any data irregularities before you submit the data to a regulatory authority.

Automation can help minimize fraud risk too. Using AI and ML can help flag suspicious activities and trigger alerts. As this study by Deloitte explains:

“Machine learning can also analyze big data more efficiently, build statistical models quickly, and react to new suspicious behaviors faster.”

Using traditional methods (like RPA) for fraud detection requires creating manual rules. RPA works well in a structured data environment. But given the high volume of complex data in banking, you’ll need ML systems for fraud detection.

Blanc Labs’ Banking Automation Solutions

Blanc Labs helps banks, credit unions, and Fintechs automate their processes. We tailor-make automation tools and systems based on your needs. Our systems take work off your plate and supercharge process efficiency.

Our team deploys technologies like RPA, AI, and ML to automate your processes. We integrate these systems (and your existing systems) to allow frictionless data exchange.

Book a discovery call to learn more about how automation can drive efficiency and gains at your bank.

Many businesses are curious about this document automation process because, just like you, they may have heard about how it simplifies complex document layouts, captures data and organizes it for a seamless workflow.

In this article, we will explore:

What Is Intelligent Document Processing?

How Intelligent Document Processing works

Benefits of Intelligent Document Processing

What Is Intelligent Document Processing?

Intelligent document processing uses Artificial Intelligence (AI), Machine Learning (ML), Optical Character Recognition (OCR), computer vision, and Intelligent Character Recognition (ICR) to automate data extraction from complex semi-structured and unstructured documents. This technology helps you categorize the extract data into a meaningful format that is easier for people or a system to comprehend. A popular use case for intelligent document processing is mortgage origination and decisioning, where applications can run into hundreds of pages.

Read more on how Intelligent Document Processing helps financial services organizations.

How Does Intelligent Document Processing Work?

IDP uses deep-learning AI technology to scan complex data, extract it and organize it into predefined categories. The best part is that this technology can be trained in up to 190 languages.

One of the best ways to understand how document processing works is to look into a few use cases first. Here are multiple ways in which IDP helps organizations from various industries to automate their data.

IDP for Human Resources

One of the popular intelligent document processing use cases is human resources. This paper-intensive industry has already transitioned to data automation by:

Screening resumes and capturing the right skill sets that match a job description. This has helped HR teams avoid going through resumes manually and narrow down on candidates who are fit to take up the role, hassle-free.

Keeping all the employee data in one place. Earlier, HR teams were forced to manage hundreds of thousands of files for new and existing employees. Not only was it hard to find specific data quickly, but it was hard to comprehend at times. But with IDP, it is easier to update and extract the employee data when need be.

Simplifying the employee onboarding process by capturing employee information based on the forms filled in by them.

IDP for Mortgage Processing

Another data heavy use case you can refer to is mortgage processing. Given how vast the industry is, you can only imagine the number of documents that accumulate at every stage of the mortgage process. Let’s see how IDP simplifies document accumulation and data extraction for this industry:

IDP is capable of processing high-volume mortgage data and identifying possible risks one may face during the process. With IDP, mortgage officers can identify the cause for rejection and inform approvers about these potential risks.

Validating documents is time consuming. However, IDP helps you validate the data from documents with a button and offers you insights on whether to move ahead with the mortgage or not.

You can also audit each mortgage application with IDP and that too without human intervention. It can be time consuming to audit documents for a mortgage even when you have a professional helping you out with the process. With IDP, you can save time and also check the authenticity of each document.

Top 7 Benefits of Intelligent Document Processing

Increases Employee Productivity

One of the benefits of using IDP is its ability to increase employee productivity. Intelligent document processing helps employees free up their time that they spend on doing repetitive tasks such as data entry and record management. Lesser time spent on repetitive tasks helps increase their productivity.

Helps Reduce Manual Work

IDP is also known for reducing manual work as it enables extraction of data from a document, an image, sound, or even a video using its AI technology. What’s more, the data extracted is then transformed into text, thereby helping employees reduce manual work on such tasks. It uses Natural Language Processing (NLP) that understands the content and converts that data into text.

Automates Classification of Documents

Once the data is converted to text, it is classified into different categories, without the need for human intervention. This helps your organization with data collection and streamlining the document management process with minimal errors.

Enables the Processing of Large Volumes of Documents

Another benefit of using IDP is processing large volumes of documents in one go. While humans take time to extract data from each document, the same isn’t true in the case of IDP. Unlike humans, a document processor can extract data from multiple documents simultaneously. You can tackle a giant database and avoid spending capital on a data entry team.

Improves Data Accuracy

Humans are prone to make errors when feeding data to a database, especially when there are a large number of documents. This may hamper the overall authenticity of the database and may leave managers questioning its accuracy.

Thankfully, the same isn’t true in the case of AI and ML-based IDP technology. It is capable of entering the data accurately in the database and retrieving the same data with speed when its users need it on an urgent basis. In short, an automated document processor can extract accurate data and eliminate mistakes with an accuracy of more than 90%.

Increases User and Customer Satisfaction

Intelligent Document Processing is capable of providing users with optimal responsiveness through the life cycle of work to be performed. With IDP, you can process evidentiary documents, extract the right keywords from a data set in less time. What’s more, the automated process can use keywords to route emails to the right department for faster throughput from start to finish. This helps speed up the response time between receiving an origination request to approving it, from a claim initiation to notification of completion, etc. Documents are no longer the bottleneck.

Offers Data Security

When documents are managed manually or in disparate data systems, there is always a possibility of a data breach. But with IDP, documents can be kept in a secure, centralized location. This enables businesses to be more compliant with data protection regulations. In other words, you can make sure that the data saved never gets misused by anyone.

Maximize the Benefits of Intelligent Document Processing