Blanc Labs Welcomes Two New Leaders to Advance AI Innovation and Enhance Tech Advisory Services for Financial Institutions Across North America

May 7, 2024

May 6 (Toronto, ON)— Blanc Labs, a pioneer in Lending Technology, Artificial Intelligence (AI) and Intelligent Automation, is thrilled to announce the appointment of two new members to its executive team, Prithvi Srinivasan and Ali Khachan, both distinguished leaders in technology and consulting.

Prithvi Srinivasan, a former Partner at Deloitte Consulting, is joining Blanc Labs as the Managing Director for Advisory Services. Prithvi brings a wealth of expertise in technology strategy, digital transformation, and business operations excellence, and specializes in driving mission-critical transformation programs. Leveraging his extensive experience in aligning technology initiatives with business value, Prithvi is set to propel financial institutions forward using Blanc Labs’ expertise in lending technology, AI, and intelligent automation. His proven track record in driving successful enterprise transformations and optimizing technology estates underscores his commitment to fostering innovation and delivering value to clients. Prithvi excels in transforming complex strategies into actionable successes, ensuring technology not only meets but advances business objectives.

Ali Khachan, a tech startup leader and former Principal at Boston Consulting Group (BCG), joins Blanc Labs as Managing Director of AI. As a strategic operator with over 15 years of leadership at the nexus of technology and business, Ali has demonstrated a keen ability to drive transformational growth through AI and digital innovations. His expertise in scaling up ventures, spearheading digital transformations, and maximizing value creation for global enterprises will play a pivotal role in shaping the future of Blanc Labs as it continues to pioneer groundbreaking AI solutions.

“The addition of Prithvi and Ali to our executive team significantly strengthens Blanc Labs’ strategic capabilities and reinforces our position as a leading technology partner for the financial sector,” said Hamid Akbari, CEO of Blanc Labs. “Their exceptional expertise and visionary leadership will accelerate our strategic initiatives across Advisory Services, Data, Automation, Artificial Intelligence, and Generative AI solutions. I am confident that with Prithvi and Ali on board, Blanc Labs will achieve new heights in delivering exceptional value to our clients and shaping the future of digital transformation in the financial services industry.”

Both Prithvi and Ali will be speaking at the Canadian Lenders Association Bankers Summit in Toronto on May 15th. They will conduct a series of workshops focused on AI in Lending, demonstrating Blanc Labs’ commitment to fostering knowledge exchange and leading the charge in AI solutions for financial services. To register for the workshops, please reach out to Blanc Labs through their website.

ABOUT BLANC LABS

Blanc Labs is a preferred partner for enterprises looking to digitize and build the next generation of technology products and services. To help companies rapidly deliver on their digital initiatives, Blanc Labs has developed expertise and bespoke solutions in a wide variety of applications in financial services, healthcare, enterprise productivity, and customer experience. Headquartered in Toronto, Blanc Labs serves the Americas through operations in Toronto, New York, Bogota, and Buenos Aires. For more information on how Blanc Labs is building a better future, visit www.blanclabs.com.

Financial Services | AI | Banking Automation | Digital Banking | Lending Technology

How to Automate Loan Origination Systems

May 1, 2023

Loan origination automation is critical because the loan origination process is labor-intensive and prone to human error.

Translation?

The process takes expensive human capital that you can dedicate to other, more strategic tasks. It’s also prone to human error, which increases your costs and puts your reputation at risk.

Automating the process takes humans out of the equation, minimizing the cost of human capital and the risk of human error.

In this article, we explain how to automate the process using an automated loan origination system.

What is the Loan Origination Process?

Loan origination is the process of receiving a mortgage application from a borrower, underwriting the application, and releasing the funds to the borrower or rejecting the application.

When a customer applies for a mortgage, the lender initiates (or originates) the process necessary to determine if a borrower should be lent funds according to the institution’s policies.

The process is extensive and takes an average of 35 to 40 days. The origination process involves five steps, as explained below.

Prequalification

Prequalification is a screening stage. This is where lenders look for potential reasons that can adversely impact a borrower’s capability to repay the loan.

Typically, lenders look for things like:

Income: Does the borrower make enough money to be able to service the loan payments, and is that income consistent?

Assets: Should the borrower’s income stop for some reason; do they have enough assets to remain solvent given their existing liabilities?

Debt: Is the borrower overleveraged? Are the debts secured or unsecured?

Credit record: Has the buyer made loan payments on time in the past?

These factors help the lender determine if they should spend time processing the application further.

Preparing a Loan Packet

Lenders create a packet (essentially a file of documents) for prequalified borrowers.

The packet includes the borrower’s documents, including KYC, financial statements, and other relevant documents that provide an overview of the borrower’s debt servicing capability.

Lenders also include documents that highlight the reasons that make an applicant eligible or ineligible to be considered for the loan.

For example, the lender may include the borrower’s debt-to-income ratio, properties and assets at market value, and income streams to provide an overview of whether the borrower is a good candidate for the loan.

Some lenders take extra steps to double-check the applicant’s claims.

For example, lenders might hire a valuer or research property rates to verify your real estate investment’s current market value. The valuer’s report is added to the packet for the underwriter’s reference.

Negotiation

Many borrowers, especially those with an excellent credit record, browse their options before accepting a lender’s offer.

The borrower might want to negotiate a lower rate or ask for a fixed rate instead of a floating rate.

Term Sheet Disclosure

A term sheet is a summary of the loan. It’s a non-binding document that contains the terms and conditions of the mortgage deal.

The term sheet includes the tenure, interest rate, principal amount, foreclosure charges, processing fees, and other relevant details.

Loan Closing

If the negotiations go well and the borrower accepts the offer, the lender closes the loan.

The lender creates various closing documents, including final closing disclosure, titling documents, and a promissory note.

The borrower and lender sign the documents, and the lender disburses the funds as agreed.

3 Ways to Automate Loan Origination

Now that you know the loan origination process, let’s talk about automating parts of this process to make it more efficient.

Digitizing Loan Applications

You can create an online portal where applicants can initiate a loan application and upload their KYC and other documents.

The documents are automatically transferred to your internal systems for prequalifying the applicant.

IDP extracts and relays the applicant’s data from the documents to your system.

Once the data is in the system, robotic process automation (RPA) can be used to determine if an applicant should be prequalified.

You can use a machine learning (ML) algorithm for deeper insights.

ML can help identify characteristics that make a person more or less likely to service the loan until the end of the term, allowing you to make smarter decisions.

Assembling Loan Documentation

Cloud-based RPA can collect documents from the online portal and organize them in one location. Not only are digital copies faster to collect, but they’re easy to store and search.

Think about it. You’ve received an application, but it’s missing the cash flow statement for last year. You’ll need to email or call the applicant to upload the documents, wasting your and the applicant’s time.

Lenders typically have a document checklist. Automating checklists is easy with RPA — when the applicant forgets to upload a document, the RPA can trigger notifications to the applicant.

The system can also notify the loan officer if the applicant becomes non-responsive.

Speeding Up Underwriting

Borrowers want faster access to funds, but lenders must complete their due diligence.

Lending automation can help reduce the time between application and approval.

With technologies like artificial intelligence (AI), ML, and RPA, automation systems can assess an applicant’s creditworthiness within seconds.

RPA can help with basics like checking the minimum credit score and income levels. RPA can also flag any areas that indicate greater risk, such as excessive variability in the applicant’s cash flows.

Moreover, loan origination is a compliance-heavy process. It’s easy to forget a small step when you’re overwhelmed with loan applications.

RPA ensures all compliance steps are taken care of. If they’re not, the system can trigger alerts for the underwriter as well as the superiors.

AI and ML can provide deeper insights. These technologies can use big data to identify patterns that make a borrower more likely to default, allowing you to make smarter decisions fast.

Moreover, AI and ML can help you look beyond credit scores and find people that are more creditworthy than their credit scores suggest.

As Dimuthu Ratnadiwakara, assistant professor of finance at Louisiana State University, explains:

“Traditional models tend to lock anyone with a low credit score—including many young people, college-educated people, low-income people, Black and Hispanic people and anyone who lives in an area where there are more minorities, renters and foreign-born—out of the credit market.”

How Shortening Loan Origination With Automation Helps

Shortening the loan origination process benefits you in multiple ways:

Match customer expectations: You’ll deliver on the customers’ expectations by offering faster loan processing. 40% of mortgage customers are willing to complete the entire process using self-serve digital tools, but 67% still interact with a human representative via phone.

Deliver better experiences: Automation offers various opportunities to improve customer experience. For example, you can set up an AI chatbot that responds to customers’ questions in real time.

Increase efficiency: You can process more applications per month by automating loan origination.

Better use of your staff’s time: Automated workflows allow credit officers to focus on parts of the business that require a human touch, such as building stronger relationships with clients, than on repetitive tasks that automation can perform more accurately.

Loan Origination Automation with Blanc Labs

Selecting the right partner to set up loan origination automation is critical. Partnering with Blanc Labs ensures frictionless implementation of a personalized loan origination system.

Blanc Labs tailor-makes solutions best suited for your needs and workflow. Blanc Labs starts by assessing your needs and creating a strategy to streamline your loan origination processes. Then, Blanc Labs creates an automation system using technologies like RPA, AI, and ML.

Book a demo to learn how Blanc Labs can help you automate your loan origination workflow.

What is Open Banking and Is It Available in Canada?

Financial Services | Digital Banking | Digital Transformation | Lending Technology | Open Banking

What is Open Banking and Is It Available in Canada?

February 9, 2023

If you’re a bank or financial institution, you should know what open banking is. Open banking consolidates your customers’ financial information. It allows them to access their financial data via a single banking or third-party app, allowing them to make smarter and faster financial decisions.

This guide explains open banking, how it works, and its benefits.

What Does Open Banking Mean?

Open banking is a secure framework that facilitates the exchange of financial data between financial institutions and third parties through APIs (application programing interface).

Think about the last time you wanted to check your investment portfolio. You probably had to log into multiple online portals and bank accounts to get financial information.

Open banking (also known as consumer-directed or consumer-led banking) can shorten this process to a few minutes by bringing all the information to a single dashboard.

When you try to access financial information via a fintech app with open banking, your bank transmits data via a secure online channel to the app. More importantly, you don’t need to provide login credentials when using open banking.

As you can imagine, being able to pull financial data securely from banks and other institutions will allow fintechs and the banks themselves to develop innovative products that enable Canadians to manage finances more effectively.

How Open Banking Works

Here is a typical scenario for how open banking works:

A bank’s customer downloads a fintech app to manage finances and wants to start using it.

The app needs to access financial data, so it prompts the customer to link their bank accounts.

The customer authorizes the bank to securely share financial data with the app.

The bank transmits customer data through a secured online channel.

The app provides financial insights and recommendations.

Isn’t that how apps operate anyway?

Well, yes, except for one key difference. Traditionally, when a person links an app to their bank account, it uses screen scraping and the person’s login credentials to log into it and pull financial data.

On the other hand, open banking uses APIs (application programming interfaces). In simple terms, APIs allow two systems (the banking system and the third-party app, in this case) to communicate and exchange information securely.

Banks or financial institutions are responsible for building, implementing and managing the APIs that will allow customers to connect their accounts with new and innovative apps.

Screen scraping is prone to privacy and security risks since you can’t control how the fintech stores or uses your data. The practice can also violate your bank’s electronic access agreement (EAA), which frees the bank of any liability in case of an unauthorized transaction in your account.

Screen scraping will likely become obsolete once open banking becomes available in Canada.

What is Screen Scraping?

Screen scraping is the process of capturing data present on a screen — from a webpage, document, or app — for using it in another system or app.

It’s generally used by apps that need to extract data from legacy systems that lack an API management system or any other source of data extraction.

Data accessed by apps through screen scraping isn’t regulated. Without a standardized system, all third parties use their own level of security and approach to handling data.

Screen scraping platforms also store login credentials as text strings. The lack of encryption leaves your data vulnerable to attacks from hackers.

Unfortunately, an estimated four million Canadians are accessing banking-style services via screen scraping. The growing popularity of financial planning apps strongly calls for a more secure, regulated framework like open banking.

However, open banking still has its limitations. For example, the bank might securely transmit the information to a third party, but if someone hacks the app itself, they might steal your data. So even though open banking is safer than screen scraping, it’s not fully secure.

Benefits of Open Banking

The implementation of open banking in Canada will benefit both you and your customers.

Here are four ways open banking will benefit your customers:

Gives an overview: Open banking provides a secure framework to pull information from your bank accounts, credit cards, investment partners, and other financial institutions. An open banking app can consolidate all your financial data and provide a complete overview in one place without switching between websites and manually extracting information.

Allows shopping around for the best deal: Comparing deals for personal loans, credit cards, or mortgages requires careful research. A comparison app using open banking can speed up the process and help you find the best deal. Apps can also help you understand how likely you are to qualify if you apply for a loan based on your financial information.

Speeds up the application process: Applying for loans or credit requires submitting information, including your financial statements and KYC documents. Instead of manually submitting these documents, an app can store them for you and submit them as necessary when applying for a loan or opening an investment account.

Helps make smarter financial decisions: Fintech apps can use artificial intelligence (AI) and machine learning (ML) to create financial roadmaps based on your financial data. You can use these apps to create a budget, understand your spending habits, and find the best investment options based on your risk appetite. Apps may also project cash flows based on your budget and financial obligations so that you can estimate the available balance in your account at the end of each month.

Here are four ways open banking benefits you as a bank or financial institution:

Collaborate with third parties: Collaborating with third-party apps can help you explore data-sharing agreements and identify new opportunities. You can streamline processes and offer more related services to stay ahead of the competition.

Prepare for the future: Open banking isn’t available in Canada, but it soon will be. Over time, your customers will likely demand the privacy and security that open banking offers. As data privacy laws evolve, open banking will ensure you’re in an excellent position to adapt to changes. Moreover, quickly becoming compliant with evolving rules without interrupting service improves customer experience.

Increase market share: Your customers crave convenience. Allowing them to consolidate financial information securely ensures excellent customer experience. Offering open banking is critical to fulfilling your customer’s demands. Over time, you might even lose market share by not offering open banking.

Lower operating costs: Open banking ensures banks’ data lives in a centralized, digitally accessible location. This minimizes data silos and facilitates automation. Automating banking processes like mortgage underwriting allows you to reduce operating costs.

The Canadian government is working on safely implementing open banking in Canada. The government appointed Abraham Tachjian to lead Canada’s open banking framework development initiative in March 2022.

However, the government is committed to implementing open banking at the earliest and realizes the benefits it can offer to Canadians.

For example, when asked about how open banking can address the challenges facing BIPOC Canadians, small businesses, and rural/remote communities, Tachijan explained:

“While Canada’s banking framework aims to ensure all Canadians have access to basic bank accounts, some Canadians may be underbanked. Open Banking creates the opportunity for consumer-led banking, which gives consumers and businesses greater control and protection over their financial data, as well as more transparency on how it’s used.”

While the government lays the groundwork to implement open banking, you should ensure you have everything set up to offer customers open banking soon after it becomes available in Canada.

Is Your Financial Institution Ready for Open Banking?

Open banking is about to transform the financial services industry. Your customers will have the flexibility to choose how they interact with your bank, and your competitors will have the option to offer innovative solutions.

Implementing open banking can feel daunting, but partnering with the right team can simplify the process.

Blanc Labs helps banks implement open banking from scratch. Book a discovery call to learn more about our open banking solutions.

Many businesses are curious about this document automation process because, just like you, they may have heard about how it simplifies complex document layouts, captures data and organizes it for a seamless workflow.

In this article, we will explore:

What Is Intelligent Document Processing?

How Intelligent Document Processing works

Benefits of Intelligent Document Processing

What Is Intelligent Document Processing?

Intelligent document processing uses Artificial Intelligence (AI), Machine Learning (ML), Optical Character Recognition (OCR), computer vision, and Intelligent Character Recognition (ICR) to automate data extraction from complex semi-structured and unstructured documents. This technology helps you categorize the extract data into a meaningful format that is easier for people or a system to comprehend. A popular use case for intelligent document processing is mortgage origination and decisioning, where applications can run into hundreds of pages.

Read more on how Intelligent Document Processing helps financial services organizations.

How Does Intelligent Document Processing Work?

IDP uses deep-learning AI technology to scan complex data, extract it and organize it into predefined categories. The best part is that this technology can be trained in up to 190 languages.

One of the best ways to understand how document processing works is to look into a few use cases first. Here are multiple ways in which IDP helps organizations from various industries to automate their data.

IDP for Human Resources

One of the popular intelligent document processing use cases is human resources. This paper-intensive industry has already transitioned to data automation by:

Screening resumes and capturing the right skill sets that match a job description. This has helped HR teams avoid going through resumes manually and narrow down on candidates who are fit to take up the role, hassle-free.

Keeping all the employee data in one place. Earlier, HR teams were forced to manage hundreds of thousands of files for new and existing employees. Not only was it hard to find specific data quickly, but it was hard to comprehend at times. But with IDP, it is easier to update and extract the employee data when need be.

Simplifying the employee onboarding process by capturing employee information based on the forms filled in by them.

IDP for Mortgage Processing

Another data heavy use case you can refer to is mortgage processing. Given how vast the industry is, you can only imagine the number of documents that accumulate at every stage of the mortgage process. Let’s see how IDP simplifies document accumulation and data extraction for this industry:

IDP is capable of processing high-volume mortgage data and identifying possible risks one may face during the process. With IDP, mortgage officers can identify the cause for rejection and inform approvers about these potential risks.

Validating documents is time consuming. However, IDP helps you validate the data from documents with a button and offers you insights on whether to move ahead with the mortgage or not.

You can also audit each mortgage application with IDP and that too without human intervention. It can be time consuming to audit documents for a mortgage even when you have a professional helping you out with the process. With IDP, you can save time and also check the authenticity of each document.

Top 7 Benefits of Intelligent Document Processing

Increases Employee Productivity

One of the benefits of using IDP is its ability to increase employee productivity. Intelligent document processing helps employees free up their time that they spend on doing repetitive tasks such as data entry and record management. Lesser time spent on repetitive tasks helps increase their productivity.

Helps Reduce Manual Work

IDP is also known for reducing manual work as it enables extraction of data from a document, an image, sound, or even a video using its AI technology. What’s more, the data extracted is then transformed into text, thereby helping employees reduce manual work on such tasks. It uses Natural Language Processing (NLP) that understands the content and converts that data into text.

Automates Classification of Documents

Once the data is converted to text, it is classified into different categories, without the need for human intervention. This helps your organization with data collection and streamlining the document management process with minimal errors.

Enables the Processing of Large Volumes of Documents

Another benefit of using IDP is processing large volumes of documents in one go. While humans take time to extract data from each document, the same isn’t true in the case of IDP. Unlike humans, a document processor can extract data from multiple documents simultaneously. You can tackle a giant database and avoid spending capital on a data entry team.

Improves Data Accuracy

Humans are prone to make errors when feeding data to a database, especially when there are a large number of documents. This may hamper the overall authenticity of the database and may leave managers questioning its accuracy.

Thankfully, the same isn’t true in the case of AI and ML-based IDP technology. It is capable of entering the data accurately in the database and retrieving the same data with speed when its users need it on an urgent basis. In short, an automated document processor can extract accurate data and eliminate mistakes with an accuracy of more than 90%.

Increases User and Customer Satisfaction

Intelligent Document Processing is capable of providing users with optimal responsiveness through the life cycle of work to be performed. With IDP, you can process evidentiary documents, extract the right keywords from a data set in less time. What’s more, the automated process can use keywords to route emails to the right department for faster throughput from start to finish. This helps speed up the response time between receiving an origination request to approving it, from a claim initiation to notification of completion, etc. Documents are no longer the bottleneck.

Offers Data Security

When documents are managed manually or in disparate data systems, there is always a possibility of a data breach. But with IDP, documents can be kept in a secure, centralized location. This enables businesses to be more compliant with data protection regulations. In other words, you can make sure that the data saved never gets misused by anyone.

Maximize the Benefits of Intelligent Document Processing

Benefits such as these (and others discussed in the article above), will help you identify various reasons why a data extraction processes like Intelligent Document Processing are essential for your business. Once you decide to opt for intelligent document processing, it’s time to look for the right implementation partner.

Automate workflows for document collection, digitization and analysis

Replace manual effort through intelligent data capture

Connect with third party data providers for analysis and insights

Analyze document data, provide status alerts, and flag fraudulent entries

Secure documents in a drop box

Deploy on premises, in the cloud or as a hybrid model

We hope that learning about these benefits will help you arrive at a decision faster and invest in the best document processing solution in the market.

Currently, most enterprises have a workflow rampant with manual document-heavy processing.

However, businesses are quickly digitizing their document-processing workflows. 50% of B2B invoices across the globe will be processed without manual intervention according to a Gartner study. The reason? Manual document processing is more expensive than the cost of the documents themselves.

For example, the average cost of processing a single invoice was $10.89 in 2021. Manual document processing is also prone to human errors like fat finger errors. In a world where 90% of the data is unstructured, you need a tool that can automatically convert unstructured data into structured data to supercharge your productivity.

This guide explains how you can use intelligent document processing to save your business plenty of money, time, and resources.

What is Intelligent Document Processing?

Intelligent Document Processing (IDP) is a technology that automatically extracts unstructured data from multiple document sources, including images, online forms, and PDFs. IDP is also known as Cognitive Document Processing (CDP).

IDP converts this unstructured data into structured data using multiple technologies, including natural language processing (NLP), machine learning (ML), optical character recognition (OCR), and intelligent character recognition (ICR). Together, these technologies make IDP intelligent.

OCR is often used interchangeably with IDP. However, that’s not true. IDP uses OCR as one of the technologies to extract data.

How Does Intelligent Document Processing Work?

Here’s how a document is processed using IDP:

Conversion: An IDP platform starts by capturing your document through a scanning device. Once it converts a physical document into a digital one, it starts ingesting data.

Document image processing: The document’s image is processed for optimal OCR and archival.

Reading text using OCR: OCR helps the machine accurately read the scanned document’s text.

Identify language elements with NLP: IDP platforms use NLP to find language elements using methods like feature-based tagging and sentiment analysis.

Extracting elements using AI: IDP uses AI to extract information elements like contact numbers, addresses, and names.

Validation: IDP platforms validate information using third-party databases and lexicons for data validation. Data points are flagged when the platform can’t validate them so someone from the team can review them manually.

Top Intelligent Data Processing Use Cases in Banking

Reading and writing financial documents make up a large portion of a bank’s workflow. As a bank, you need to process data fast to offer best-in-class services to your customers without making errors.

IDP helps banks guarantee accuracy and efficiency to their clients. In addition to data extraction’s key role in a bank’s workflow, banks can also use IDP platforms for fraud detection.

Here are some of the most common use cases of IDP for banks.

Mortgage Underwriting

Customer satisfaction with mortgage originators reduced by five points on a 1,000-point scale in 2021 according to a study by J.D. Power driven by record mortgage origination volume. Banks need to automate their mortgage workflow to scale as the demand grows. After all, customer satisfaction is one of the most significant differentiators in the mortgage industry.

The mortgage workflow involves collecting various documents. Extracting data from these documents is one of the major factors slowing down the workflow. This is where an IDP tool can help streamline your mortgage workflow.

An IDP tool helps you speed up the underwriting process with automation. It automatically reads and extracts relevant data and relays it to your bank’s credit evaluation system.

However, the claims processing workflow can be complex. Claims data comes in various formats—customers might send data as word files, PDFs, and images. Plus, you might receive the data via multiple channels—you might receive it via email, chat, or over a call.

Unifying this data without manual effort is a massive challenge. Traditionally, banks used OCR to process physical documents. However, the lack of accuracy required manual review.

An IDP tool is a great alternative to OCR for claims processing. Thanks to technologies like NLP, computer vision, and deep learning, it provides greater accuracy than traditional OCR.

Customer Onboarding

Customer onboarding is one of the most resource-intensive processes for a bank. Banks spend an average of $280 to onboard a single client according to Backbase—the cost can add up when you’re onboarding hundreds or thousands of customers every month.

Many of these expenses go towards processing documents, including the bank’s forms, credit reports, or tax returns. Sure, you can try automating this workflow. However, the automation will break down as soon as a new document type is introduced or you change your form’s template.

An IDP tool can help tame your customer onboarding costs. Your customers will appreciate a fast onboarding experience, and you’ll save money, increase productivity, and make an excellent first impression.

Financial Document Analysis

Banks handle thousands of financial documents every day. From financial statements to tax returns, carefully studying financial documents is critical to a bank’s operations.

Financial analysis is a cognitively heavy task. Why make your team spend time on mundane tasks like manipulating data when you can use an IDP tool to automate this process and enable your team to concentrate on their more complex deliverables.

Using an IDP tool helps analysts automatically structure and populate relevant financial data into their system. You’ll do your analyst team a favor by eliminating a lot of their manual work, allowing them to focus on analysis.

KYC Process Automation

KYC (Know Your Customer), Re-KYC, and C-KYC are critical for compliance. Banks might need to refer to a customer’s KYC details at various stages during a customer’s journey.

However, handling hand-written KYC forms is a hassle. Migrating a customer’s KYC data comes with challenges like human error and work overload. Committing errors when underwriting a mortgage or onboarding a customer costs money, but failing to comply with KYC requirements may increase the legal, compliance and regulatory risks.

Using IDP ensures accuracy, so you never have to lose your reputation and pay a fine for failing to comply with KYC norms. The McKinsey KYC Benchmark Survey found that by increasing end-to-end KYC-process automation by 20%, an organization could enjoy the following positive outcomes:

Increased quality assurance by 13%

Improved customer experience (by reducing customer outreach frequency) by 18%

Increased the number of cases processed per month by 48%

The Bottom Line

Banks process a colossal amountnumber of documents and data each day. Getting new customer data into the system, processing claims, and analyzing financial statements are heavily data-driven tasks that involve dozens of documents from hundreds of customers.

The probability of committing errors is high. Banks also need a large team just to process documents and structure the data in those documents.

Banks need an IDP tool to automate this process and remove the risk of error from the process. It also integrates with applications to make migrating the data easier. An IDP tool also validates data and alerts team members in exception cases, when it requires a human to review accuracy.

It is important to select an IDP tool that offers the right solutions for your industry. Better yet, find a partner who can create a custom IDP solution tailor-made for you.

Blanc Labs partners with financial organizations like banks, credit unions, and fintechs to automate operations.

We can help you create robust automation solutions that minimize manual effort, reduce errors, and improve productivity. Our team helps you use the most advanced technologies including AI and ML to automate complex, resource-heavy processes like document processing.

Book a discovery call with us if your financial organization deals with plenty of documents daily. We’ll come up with a tailor-made solution to minimize the friction in your document processing workflow.

Transforming a Bank’s Value Network with Automation

Transforming a Bank’s Value Network with Automation

August 11, 2022

Michael Porter’s value chain has been one of the top seminal business management ideas that saw business operations with through a new lens. Just like the value chain resulted in concepts like value creation and value pricing leading to phenomenal growth in global business scale and operations in the last 50 years, we are now seeing a similar scenario in the financial services industry with intelligent automation.

At the turn of the century, we saw a new concept emerge that resulted in changing the business dynamics in the Y2K. This new business concept came to be known as value network, a series of interactions between individuals, entities, organizations, departments, and systems that collectively work towards benefitting the entire group or ecosystem. This new concept had an astounding impact on how businesses and markets operated and paved the course of today’s business ecosystem. For instance, the rise of Apple and its ecosystem can be attributed to this shift.

A similar shift is also taking place in the financial services industry, where the digitization, embedment, and now decentralization of the payments ecosystem with the commercialization of blockchain, cryptocurrencies, procure to pay (P2P) lending are being touted as the next big thing.

Given the pervasive technical and innovative initiatives that are emerging at breakneck speed, it is a necessity necessary to keep transforming and innovating. This is especially relevant for the financial services industry which have millennials as customers and will soon begin catering to GenZ.

To digitally transform a bank’s value network let’s start by stating the three core areas of a bank’s value network namely, network promotion & contract management, service provisioning & billing, and platform operations.

With a two-sided value network, the bank fundamentally connects a borrower with a depositor and thus, becomes the enabler of value creation for such a network. In doing so, a bank delivers core banking and back-office operations, payments and lending functions, and risk and treasury management activities.

For each of these areas, hundreds of functions and duties must be seamlessly executed with precision. Today, the increase in business volumes and scale of operations has led to bankers asking, “What if these complex and time-consuming operations can be boosted with robots (bots) assisting humans to accelerate speed, increase productivity, and assure the precision of key banking functions?”

Some of the key operational areas where bots can and, in many cases, are assisting humans to realize the true potential of an enterprise are customer service, compliance accounts payable, credit card processing, mortgage processing, fraud detection, know your customer (KYC) process, general ledger, report automation and account closure process.

By embracing bots, banks can improve the customer experience while reducing costs and improving efficiency. Increased automation combined with more efficient processes makes the day-to-day easier for teams and individual contributors as they will spend less time on tedious manual work, and more time on profitable projects. Let humans contribute to high-value innovation, and robots help in maintaining and running operations to ensure an efficient and effective enterprise. To realize the true value of bots, and for a bank to embark on its digital transformation journey, the right approach, executive sponsor, business alignment, process discovery & design, pilot, roadmap, and a center of excellence (CoE) is essential to succeed. By using tactics such as data alignment, problem framing, road mapping, and piloting new robots, a bank will be well poised to reach its automation goals.

Blanc Labs has deep industry knowledge and proven experience working with leading banks to gain efficiencies through intelligent automation solutions. We take a holistic approach, helping financial services companies build the necessary foundation and setting them up for long-term success.

Book a consultation with Blanc Labs to discover the impact of our Intelligent Automation solution.

Digital lending has evolved over the last ten years and the pandemic has only exacerbated the need for intuitive, enjoyable, dynamic, and accessible lending systems for both lenders and borrowers. In the age of Apple and Amazon, borrowers demand a seamless experience that does not involve speaking to a human being or filling out paper forms.

While traditional banks and monoline lenders are overhauling their systems to address these challenges, FinTech companies are making use of the gaps left by the big banks.

The Era of Digital Lending

According to the Canada Banker’s Association, 49% of Canadians do their banking digitally, but more importantly, 75% of Canadians intend to maintain the digital banking habits they picked up during the pandemic. Compared to five years ago, FinTech companies in the US today account for more than 38% of the personal loan space. Traditional banks, on the other hand, saw a loss of 12% of the personal loan space during the same period.

Why is this? The reason is a lack of simplicity, speed, and accessibility.

Leading FinTechs today can provide multiple quotes within minutes and fund loans within a matter of day. Apart from speed, online lenders today offer a seamless, fully digital experience as well as advanced features including security and risk assessment that does not involve a long-drawn-out credit check process.

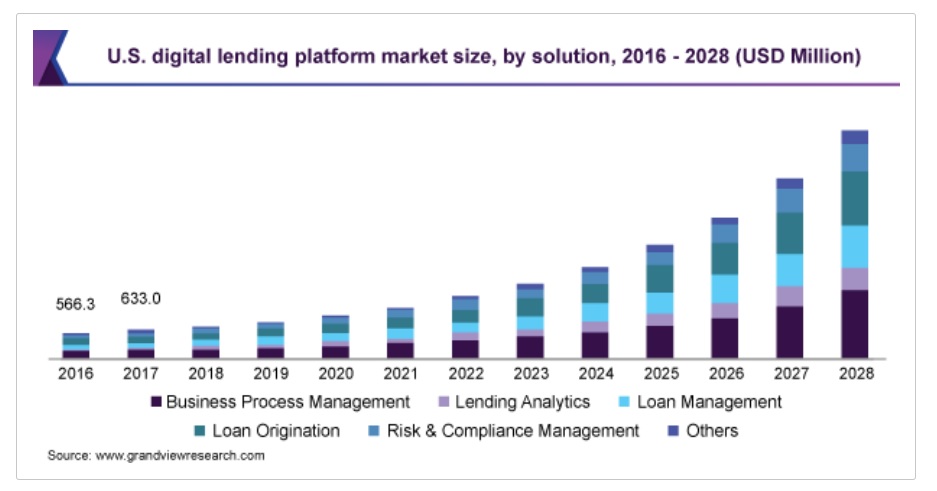

U.S. Digital Lending Platform Market Size

Digital Lending Challenges Faced by Lenders Today

Creating a fully automated, digital-first lending solution can be a complex process, especially if you don’t have the right tools and automation in place.

Automated self-service, compliance, fraud and cyber-security, document processing are just some of the many challenges that traditional financial institutions must overcome to match the experience offered by FinTechs today.

Here is our point of view on some of these key challenges:

1. Complicated and Slow Loan Origination Process

Can you think of living in a time before same-day delivery or tap payments? Neither can borrowers.

Companies that don’t offer instantaneous loan decisions run the risk of losing their customer to a FinTech that is faster and can provide quick decisions. Relying on antiquated loan origination processes that require filling multiple paper forms, visiting the bank in person, and taking days to evaluate risks and make funding decisions, will spell trouble. One study shows that 42% of respondents abandoned their applications because the process was too long and complicated, and 62% said they were unsatisfied with the digital experience, due to “too many touchpoints” and “the necessity of going to a physical location.”

Nimble FinTechs on the other hand are assessing credit risk and offering funds at the speed of light. One study by Smarter Loans found that 53% of respondents received their funds a mere 24 hours after applying for it, “suggesting that same-day-funding is becoming a standard in the industry.”

Thankfully, banks can implement digital native loan origination platforms that can automate the end to end loan origination process; or they can address bottlenecks in it like underwriting, which will make the process more streamlined for both borrowers and lenders.

2. Partial measures instead of end-to-end solutions

Delivering an end-to-end solution is a mammoth task that needs significant resources and time. The world of lending is full of large projects that took twelve to eighteen months to deliver value and this is not going to disrupt the FinTech community. Success for this is now measured in mere months. Moreover, automating one part of the customer journey and ignoring the rest can cause more complications in the long run and can re-introduce manual intervention. Instead of a piecemeal approach, consider a unified lending solution with a modular structure that addresses all steps from information collection to underwriting, servicing, and reporting. It is important to get the end state vision right first and then you can make incremental changes building towards your best customer journey if you elect to do things in recommended phases.

3. Document Intake and Data Storage

While traditional banks and brokers have been busy processing loans through paper-based or hardwired systems, FinTech companies are using automated processes to process loans faster and more transparently. Intelligent Document Processing (IDP) can automate the document intake process and apply AI (artificial intelligence) plus ML (machine learning) to extract data with more accuracy while converting unstructured data into structured data, making the data more useable. This can save you money and reduce human data entry error. In most cases, this data can be prepopulated into origination and adjudication engines to drive faster straight-through processing and time to decisioning the loan.

Productivity loss due to manual document management

4. Data Silos and Lack of Personalization

During a digital transformation project, it is important to design the system in a way that the multiple components within that system can speak to each other and convey relevant data. If for some reason this does not happen, then it simply consumes more time—time that can be used for strategizing and planning. With so many systems in silos, banks may not get a true 360-degree view of their business with a customer, therefore making it difficult to create personalized offers and recommendations for that customer. Ideally, banks should have a unified, transparent view of deposits, loans, and personal accounts if they want to keep the customer engaged and cross-sell new lending products over time to grow their share-of-wallet.

5. Regulations

Borrowers that come through the digital lending channel hand over a lot of sensitive information and so it makes good sense that lenders hardwire a regulatory compliance framework into their platform. Luckily, there are experts that can help business leaders stay on top of banking regulations and data privacy laws. The regulatory environment is rapidly changing and new industry driven changes around Open Banking are emerging as well. These dynamics are going to redefine and further embolden FinTechs, drawing clear lines around how the participants in the banking ecosystem will work together. Full assurance on regulatory reporting and compliance with industry standards is table stakes in any solution that meets this demand.

A Unified Lending Solution for Lenders

Blanc Labs provides a three-stage approach for digital lending which includes:

– Consulting assessment of your needs

– Streamlining processes and platforms

– Intelligent documentation processing (IDP)

Book a demo or discovery session with Blanc Labs to discover the impact of our digital lending solutions.