Composable Banking is a technology and transformation approach that addresses the simple fact that change is constant. To ensure that banks and FI’s can innovate swiftly and maintain the greatest level of control over their product roadmap, they must adopt a modular or “swappable” architecture. The characteristics that define Composable banking follow the MACH principles: Microservices, API First, Cloud Native, Headless.

A significant shift is underway in terms of how banks and FI’s do transformation work reflecting similar (r)evolutions in other industries like eCommerce and tech platform players like Apple and Google. The term that is being increasingly adopted to encompass a broad cross-section of tech evolution amongst financial institutions is composable banking.

Composable banking is a technology-enabled approach to delivering financial products and services to customers and ecosystem partners. It is a banking transformation approach that addresses the simple fact that change is constant. To ensure that banks and FI’s can innovate swiftly and have an agile experience roadmap, they must own a modular “swappable” architecture. This is the only way to deploy new features rapidly and retain control of their destiny.

Modular banking is not composable banking

First, let us define the characteristics of composable banking by delineating how it is different from the traditional, modular approach offered by E2E core banking systems provided by established SaaS vendors. They have been using a modular approach to extend the functionality of their core systems, whereby their propriety modules are extensible but are neither flexible nor open.

Composable banking is a solution approach that prioritizes integration readiness and flexibility, allowing organizations to dramatically improve the speed at which a company can onboard a new partner or design, build, test and deploy a new product. This is relevant for value-driven business transformations aiming to build differentiating customer experiences while setting up a future-proof, flexible and cost-effective IT landscape.

What you are Composed of matters

Composable banking is enabled through the adoption of MACH characteristics to define how an organization approaches developing and supporting technology to enable new customer experiences and improve business operations.

In the image below, we’ve highlighted some of the intended outcomes FI’s can expect to benefit from as they undertake the development of a digital transformation strategy and embark on a journey that can only be described as iterative and incremental. Spoiler alert: the work is never done. The goal though is that with investment and dedication it goes faster and gets easier to measure.

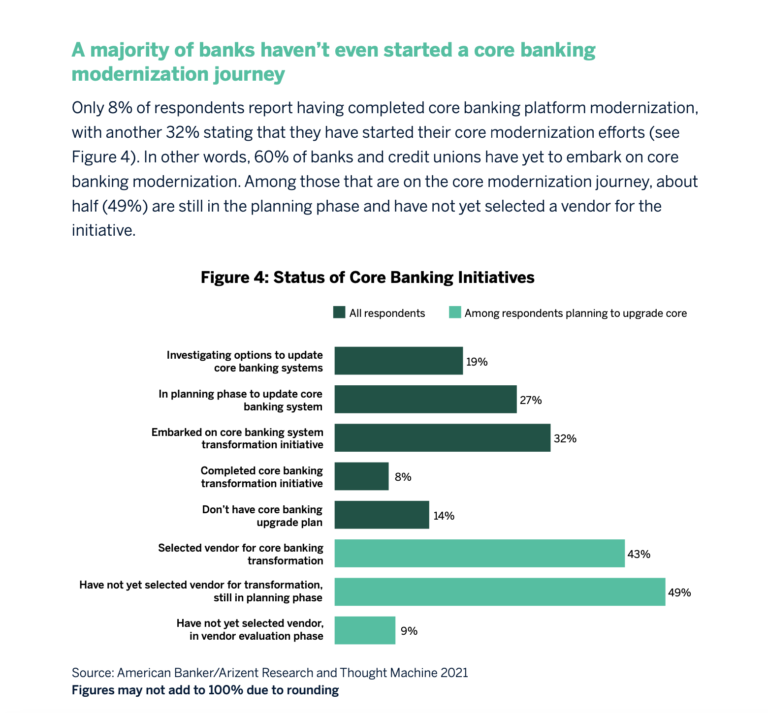

“Almost half of the global financial services organizations are still in a very early or even immature stage of their digital transformation journey.”

– Juergen Weiss, FI Practice Vice-President at Gartner

Digital Transformation is the entire journey by which a financial institution seeks to digitize and automate its processes to improve its products and customer experiences and expand into newer, untapped markets with speed and greater operating efficiency.

For those organizations that are still in the early stages of planning and prioritizing their transformation initiative, the breadth of choice, cost, and complexity can be daunting. Some of the activities required to achieve MACH characteristics require major infrastructure upgrades and the migration will most likely be implemented over a multi-year horizon.

A Composable Approach to Digital Transformation

Developing a composable transformation approach should allow for multi-threaded initiatives that support the broader organizational roadmap and transformation objectives. For this reason, we often work with clients to highlight one to two areas of opportunity, whereby organizations can see an immediate ROI in terms of CX and operational efficiency.

Initiatives like implementing an intelligent document capture platform to reduce manual data entry into a Loan Origination Systems (LOS) or conducting an API Maturity assessment allow FI’s to realize immediate benefits while building transformation capability and creating foundational progress towards a future state that reflects the characteristics of composable banking.

Curious about how you can develop a composable transformation approach at your organization? Book a workshop with Blanc Labs.

David Offierski is a tech and business strategist with a passion for innovation and customer experience. As VP of Partnerships, he is responsible for building a robust ecosystem of partners that create value for our clients and prospects.